Modeling Madrid House Prices with Linear Regression#

Requirements#

import polars as pl

import pandas as pd

import numpy as np

#import sys

from sklearn.preprocessing import OrdinalEncoder

from sklearn.model_selection import train_test_split

from IPython.display import Image

import statsmodels.api as sm

import seaborn as sns

import matplotlib.pyplot as plt

import scipy.stats as stats

import ast

from math import factorial

import itertools

from itertools import combinations

from sklearn.model_selection import KFold

import scipy

#sys.path.insert(0, 'C:/Users/fscielzo/Documents/DataScience-GitHub/EDA')

from EDA import dtypes_df, count_col_nulls, corr_matrix, outliers_table, scatter_matrix, boxplot_2D_matrix, histogram_2D_matrix, ecdf_2D_matrix, quant_to_cat

from EDA import histogram, freq_table, outlier_filter, summary, boxplot, ecdfplot, stripplot_matrix, transform_to_dummies, cross_quant_cat_summary

Conceptual description of the data#

The data set of this project contains information about Madrid houses extracted from Real State web portals.

The data has been obtained from Kaggle: https://www.kaggle.com/datasets/makofe/housesclean

The following table summarize conceptually the variables contained in the data set with which we will work along this project.

Variable Name |

Description |

Type |

|---|---|---|

|

size of the house in square meter built |

Quantitative |

|

Number of rooms of the house |

Quantitative |

|

Number of bathrooms of the house |

Quantitative |

|

Number of floors of the house |

Quantitative |

|

for detached houses, full size including house, pool, garden, etc |

Quantitative |

|

Indicates the house height |

Multiclass |

|

Indicates wether the house needs renewal or not |

Binary |

|

Indicates wether the house has lift or not |

Binary |

|

Indicates wether the house is exterior or not |

Binary |

|

higher values mean more efficient energy system |

Multiclass |

|

Indicates wether the house has parking or not |

Binary |

|

Madrid’s neighborhoods |

Multiclass |

|

Madrid’s districts |

Multiclass |

|

Indicates the house type: flat (0), chalet (1), study (2), duplex (3), top floor (4) |

Multiclass |

|

The buy price of the house |

Quantitative |

Reading the data#

First of all, we read the data.

madrid_houses_df = pl.read_csv('madrid_houses.csv')

madrid_houses_df.head()

| id | sq_mt_built | n_rooms | n_bathrooms | n_floors | sq_mt_allotment | floor | buy_price | is_renewal_needed | has_lift | is_exterior | energy_certificate | has_parking | neighborhood | district | house_type | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| i64 | i64 | f64 | i64 | i64 | i64 | f64 | i64 | i64 | bool | bool | bool | i64 | bool | i64 | i64 | i64 |

| 0 | 21742 | 64.0 | 2 | 1 | 1 | 0.0 | 3 | 85000 | false | false | true | 4 | false | 135 | 21 | 1 |

| 1 | 21741 | 70.0 | 3 | 1 | 1 | 0.0 | 4 | 129900 | true | true | true | 0 | false | 132 | 21 | 1 |

| 2 | 21740 | 94.0 | 2 | 2 | 1 | 0.0 | 1 | 144247 | false | true | true | 0 | false | 134 | 21 | 1 |

| 3 | 21739 | 64.0 | 2 | 1 | 1 | 0.0 | -1 | 109900 | false | true | true | 0 | false | 134 | 21 | 1 |

| 4 | 21738 | 108.0 | 2 | 2 | 1 | 0.0 | 4 | 260000 | false | true | true | 0 | true | 133 | 21 | 1 |

madrid_houses_df.shape

(21739, 17)

Data preprocessing#

In this section we are going to carry out some preprocessing tasks on the data.

Removing some variables#

We will remove some variables that will be not used in the project.

variables_to_remove = ['', 'id', 'district', 'neighborhood']

variables_to_keep = [x for x in madrid_houses_df.columns if x not in variables_to_remove]

madrid_houses_df = madrid_houses_df[variables_to_keep]

madrid_houses_df.head()

| sq_mt_built | n_rooms | n_bathrooms | n_floors | sq_mt_allotment | floor | buy_price | is_renewal_needed | has_lift | is_exterior | energy_certificate | has_parking | house_type |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | i64 | i64 | i64 | f64 | i64 | i64 | bool | bool | bool | i64 | bool | i64 |

| 64.0 | 2 | 1 | 1 | 0.0 | 3 | 85000 | false | false | true | 4 | false | 1 |

| 70.0 | 3 | 1 | 1 | 0.0 | 4 | 129900 | true | true | true | 0 | false | 1 |

| 94.0 | 2 | 2 | 1 | 0.0 | 1 | 144247 | false | true | true | 0 | false | 1 |

| 64.0 | 2 | 1 | 1 | 0.0 | -1 | 109900 | false | true | true | 0 | false | 1 |

| 108.0 | 2 | 2 | 1 | 0.0 | 4 | 260000 | false | true | true | 0 | true | 1 |

Data types#

We check the variables data types according to polars structure.

dtypes_df(df=madrid_houses_df)

| Columns | Python_type |

|---|---|

| str | object |

| "sq_mt_built" | Float64 |

| "n_rooms" | Int64 |

| "n_bathrooms" | Int64 |

| "n_floors" | Int64 |

| "sq_mt_allotmen… | Float64 |

| "floor" | Int64 |

| "buy_price" | Int64 |

| "is_renewal_nee… | Boolean |

| "has_lift" | Boolean |

| "is_exterior" | Boolean |

| "energy_certifi… | Int64 |

| "has_parking" | Boolean |

| "house_type" | Int64 |

Unique values#

We compute the unique values of each variable, what is useful to get a more real idea of their nature.

for col in madrid_houses_df.columns :

display(madrid_houses_df[col].unique())

| sq_mt_built |

|---|

| f64 |

| 13.0 |

| 15.0 |

| 16.0 |

| 18.0 |

| 19.0 |

| 20.0 |

| 21.0 |

| 22.0 |

| 23.0 |

| 24.0 |

| 25.0 |

| 26.0 |

| … |

| 1500.0 |

| 1600.224593 |

| 1619.87041 |

| 1700.477327 |

| 1800.379027 |

| 1930.501931 |

| 2000.0 |

| 2035.278155 |

| 2080.0 |

| 2081.332053 |

| 2199.874293 |

| 2400.0 |

| n_rooms |

|---|

| i64 |

| 0 |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| 6 |

| 7 |

| 8 |

| 9 |

| 10 |

| 11 |

| 12 |

| 13 |

| 14 |

| 15 |

| 16 |

| 18 |

| 24 |

| n_bathrooms |

|---|

| i64 |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| 6 |

| 7 |

| 8 |

| 9 |

| 10 |

| 11 |

| 12 |

| 13 |

| 14 |

| 15 |

| 16 |

| n_floors |

|---|

| i64 |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| 7 |

| sq_mt_allotment |

|---|

| f64 |

| 0.0 |

| 10.0 |

| 20.0 |

| 22.0 |

| 25.0 |

| 27.0 |

| 28.0 |

| 29.0 |

| 30.0 |

| 36.0 |

| 40.0 |

| 50.0 |

| … |

| 991.0 |

| 994.0 |

| 997.0 |

| 1000.0 |

| 2000.0 |

| 3000.0 |

| 4000.0 |

| 5000.0 |

| 6000.0 |

| 10000.0 |

| 11000.0 |

| 21000.0 |

| floor |

|---|

| i64 |

| -5 |

| -3 |

| -2 |

| -1 |

| 0 |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| 6 |

| 7 |

| 8 |

| 9 |

| 10 |

| buy_price |

|---|

| i64 |

| 36000 |

| 39000 |

| 42000 |

| 49000 |

| 49500 |

| 52000 |

| 52990 |

| 53000 |

| 54000 |

| 55000 |

| 56000 |

| 57000 |

| … |

| 6500000 |

| 6750000 |

| 6800000 |

| 6900000 |

| 7000000 |

| 7525000 |

| 7800000 |

| 7900000 |

| 8000000 |

| 8500000 |

| 8700000 |

| 8800000 |

| is_renewal_needed |

|---|

| bool |

| false |

| true |

| has_lift |

|---|

| bool |

| false |

| true |

| is_exterior |

|---|

| bool |

| true |

| false |

| energy_certificate |

|---|

| i64 |

| 0 |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| 6 |

| 7 |

| has_parking |

|---|

| bool |

| false |

| true |

| house_type |

|---|

| i64 |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

Standard encoding#

We will apply standard encoding on the categorical variables.

The variables to apply standard encoding are the following:

cols_to_std_encoding = ['house_type', 'has_parking', 'is_exterior', 'is_renewal_needed', 'has_lift']

for col in cols_to_std_encoding :

X_std_encoding = OrdinalEncoder(dtype=int).fit_transform(madrid_houses_df[[col]]).flatten()

madrid_houses_df = madrid_houses_df.with_columns(pl.Series(X_std_encoding).alias(col))

madrid_houses_df.head()

| sq_mt_built | n_rooms | n_bathrooms | n_floors | sq_mt_allotment | floor | buy_price | is_renewal_needed | has_lift | is_exterior | energy_certificate | has_parking | house_type |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | i64 | i64 | i64 | f64 | i64 | i64 | i32 | i32 | i32 | i64 | i32 | i32 |

| 64.0 | 2 | 1 | 1 | 0.0 | 3 | 85000 | 0 | 0 | 1 | 4 | 0 | 0 |

| 70.0 | 3 | 1 | 1 | 0.0 | 4 | 129900 | 1 | 1 | 1 | 0 | 0 | 0 |

| 94.0 | 2 | 2 | 1 | 0.0 | 1 | 144247 | 0 | 1 | 1 | 0 | 0 | 0 |

| 64.0 | 2 | 1 | 1 | 0.0 | -1 | 109900 | 0 | 1 | 1 | 0 | 0 | 0 |

| 108.0 | 2 | 2 | 1 | 0.0 | 4 | 260000 | 0 | 1 | 1 | 0 | 1 | 0 |

Missing values#

We check if there are missing values (null/NaN) in our data.

count_col_nulls(madrid_houses_df)

| sq_mt_built | n_rooms | n_bathrooms | n_floors | sq_mt_allotment | floor | buy_price | is_renewal_needed | has_lift | is_exterior | energy_certificate | has_parking | house_type |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| u32 | u32 | u32 | u32 | u32 | u32 | u32 | u32 | u32 | u32 | u32 | u32 | u32 |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

There are non missing values in this case.

Train-Test Split#

We perform a train-test split. Along the most part of the project we will only use the train part, since it plays the role of the data that we have in reality, and the test partition only should be used to estimate the predictive performance of the model with “new” data (estimation of future performance).

response = 'buy_price'

predictors = [x for x in madrid_houses_df.columns if x != response]

X = madrid_houses_df[predictors]

Y = madrid_houses_df[response]

X_train, X_test, Y_train, Y_test = train_test_split(X, Y, train_size=0.70, random_state=123)

X_Y_train_df = pl.concat((X_train, pl.DataFrame(Y_train)), how='horizontal')

X_Y_test_df = pl.concat((X_test, pl.DataFrame(Y_test)), how='horizontal')

EDA#

In this section we are going to complement this predictive modeling project with an exploratory data analysis.

We are going to carry out an exploratory data analysis (EDA) only on training data because of the above.

Descriptive summary#

quant_columns = ['sq_mt_built', 'n_rooms', 'n_bathrooms', 'n_floors', 'sq_mt_allotment', 'buy_price']

cat_columns = [x for x in madrid_houses_df.columns if x not in quant_columns]

quant_summary, cat_summary = summary(df=X_Y_train_df, auto_col=False,

quant_col_names=quant_columns,

cat_col_names=cat_columns)

quant_summary

| sq_mt_built | n_rooms | n_bathrooms | n_floors | sq_mt_allotment | buy_price | |

|---|---|---|---|---|---|---|

| n_unique | 689 | 17 | 15 | 6 | 304 | 2034 |

| prop_nan | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| mean | 154.019155 | 3.012683 | 2.098311 | 1.235263 | 59.190708 | 651756.495038 |

| std | 164.515279 | 1.509707 | 1.407854 | 0.710341 | 398.791114 | 776142.000602 |

| min | 13.0 | 0.0 | 1.0 | 1.0 | 0.0 | 39000.0 |

| Q10 | 55.0 | 1.0 | 1.0 | 1.0 | 0.0 | 135500.0 |

| Q25 | 70.0 | 2.0 | 1.0 | 1.0 | 0.0 | 199000.0 |

| median | 100.0 | 3.0 | 2.0 | 1.0 | 0.0 | 375000.0 |

| Q75 | 165.0 | 4.0 | 2.0 | 1.0 | 0.0 | 755000.0 |

| Q90 | 314.0 | 5.0 | 4.0 | 2.0 | 0.0 | 1550000.0 |

| max | 2400.0 | 24.0 | 16.0 | 7.0 | 21000.0 | 8800000.0 |

| kurtosis | 35.977168 | 11.227589 | 8.851221 | 11.921627 | 681.703793 | 19.434455 |

| skew | 4.454875 | 1.390361 | 2.028374 | 3.140461 | 19.343328 | 3.29838 |

| n_outliers | 1574 | 151 | 1964 | 1811 | 1003 | 1487 |

| n_not_outliers | 13643 | 15066 | 13253 | 13406 | 14214 | 13730 |

| prop_outliers | 0.103437 | 0.009923 | 0.129066 | 0.119012 | 0.065913 | 0.09772 |

| prop_not_outliers | 0.896563 | 0.990077 | 0.870934 | 0.880988 | 0.934087 | 0.90228 |

cat_summary

| floor | is_renewal_needed | has_lift | is_exterior | energy_certificate | has_parking | house_type | |

|---|---|---|---|---|---|---|---|

| n_unique | 15 | 2 | 2 | 2 | 8 | 2 | 5 |

| prop_nan | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| mode | 1 | 0 | 1 | 1 | 0 | 0 | 0 |

Outliers#

outliers_table(df=X_Y_train_df, auto=False, col_names=quant_columns)

| quant_variables | lower_bound | upper_bound | n_outliers | n_not_outliers | prop_outliers | prop_not_outliers |

|---|---|---|---|---|---|---|

| str | f64 | f64 | i64 | i64 | f64 | f64 |

| "sq_mt_built" | -72.5 | 307.5 | 1574 | 13643 | 0.103437 | 0.896563 |

| "n_rooms" | -1.0 | 7.0 | 151 | 15066 | 0.009923 | 0.990077 |

| "n_bathrooms" | -0.5 | 3.5 | 1964 | 13253 | 0.129066 | 0.870934 |

| "n_floors" | 1.0 | 1.0 | 1811 | 13406 | 0.119012 | 0.880988 |

| "sq_mt_allotmen… | 0.0 | 0.0 | 1003 | 14214 | 0.065913 | 0.934087 |

| "buy_price" | -635000.0 | 1.589e6 | 1487 | 13730 | 0.09772 | 0.90228 |

X_Y_train_df_trimmed = X_Y_train_df

for col in quant_columns:

X_Y_train_df_trimmed = outlier_filter(X_Y_train_df_trimmed, col=col, h=1.5)

Response analysis#

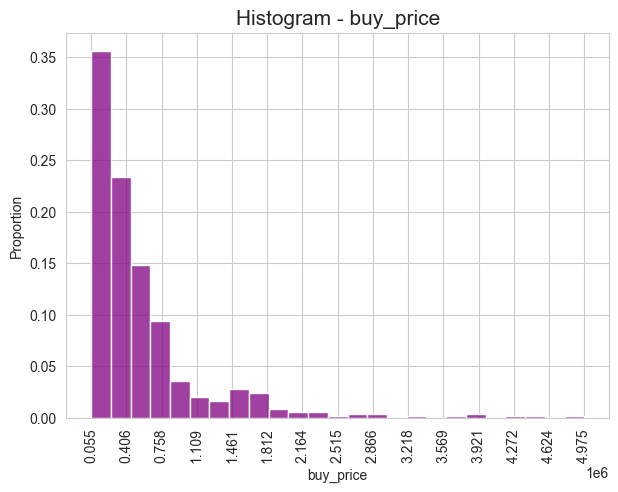

Histogram#

histogram(X=X_Y_train_df[response], bins=25, color='purple', figsize=(7,5), random=True, n=500, seed=123, x_rotation=90)

Frequencies#

response_cat = quant_to_cat(X_Y_train_df[response], rule='quartiles', n_intervals=4, random_seed=123)

freq_table(X=response_cat)

| buy_price: unique values | abs_freq | rel_freq | cum_abs_freq | cum_rel_freq |

|---|---|---|---|---|

| object | i64 | f64 | i64 | f64 |

| (-inf, 39000] | 1 | 0.0001 | 1 | 0.000066 |

| (39000, 199000] | 3829 | 0.2516 | 3830 | 0.251692 |

| (199000, 375000] | 3827 | 0.2515 | 7657 | 0.503187 |

| (375000, 755000] | 3756 | 0.2468 | 11413 | 0.750016 |

| (755000, 8800000] | 3804 | 0.25 | 15217 | 1.0 |

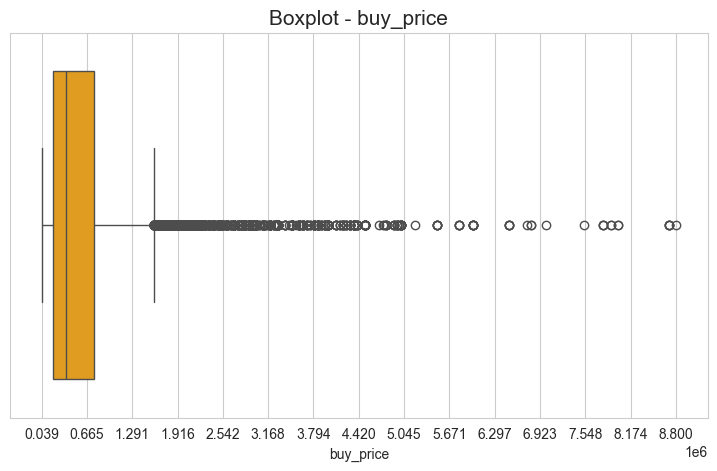

Boxplot#

boxplot(X=X_Y_train_df[response], color='orange', figsize=(9,5), n_xticks=15, x_rotation=0, statistics=False)

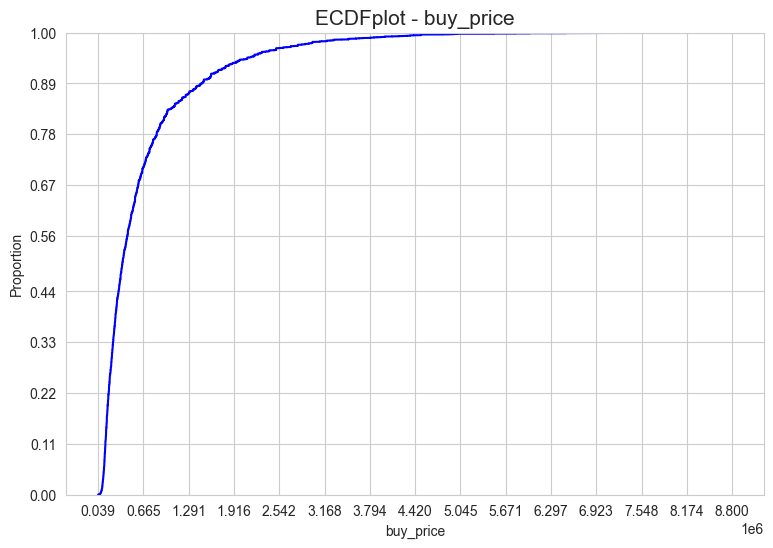

ECDF-plot#

ecdfplot(X=X_Y_train_df[response], color='blue', figsize=(9,6))

Relation between response and predictors#

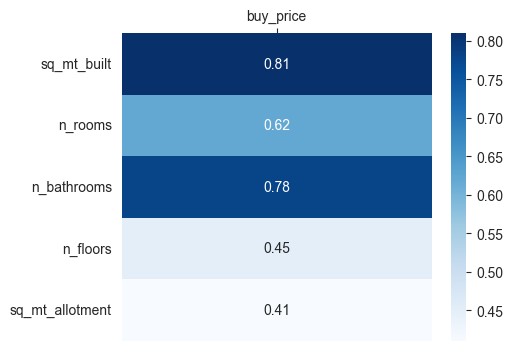

quant_predictors = [x for x in quant_columns if x != response]

cat_predictors = [x for x in cat_columns if x != response]

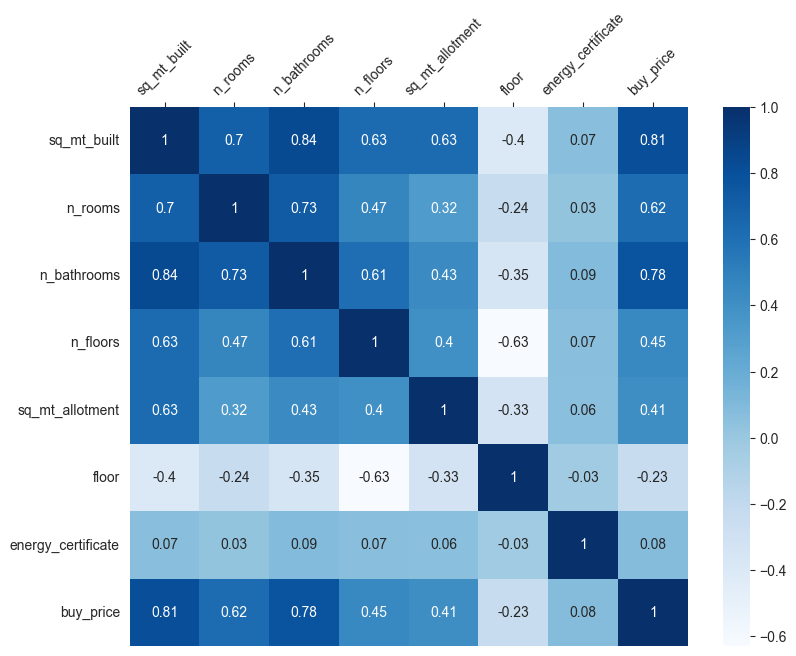

corr_matrix_response = corr_matrix(df=X_Y_train_df, response=response, predictors=quant_predictors, method='pearson')

fig = plt.subplots(figsize=(5,4))

ax = sns.heatmap(corr_matrix_response, cmap="Blues", annot=True)

ax.set(xlabel="", ylabel="")

ax.xaxis.tick_top()

ax.set_xticklabels(ax.get_xticklabels(), rotation=0)

ax.set_yticklabels(ax.get_yticklabels(), rotation=0)

plt.show()

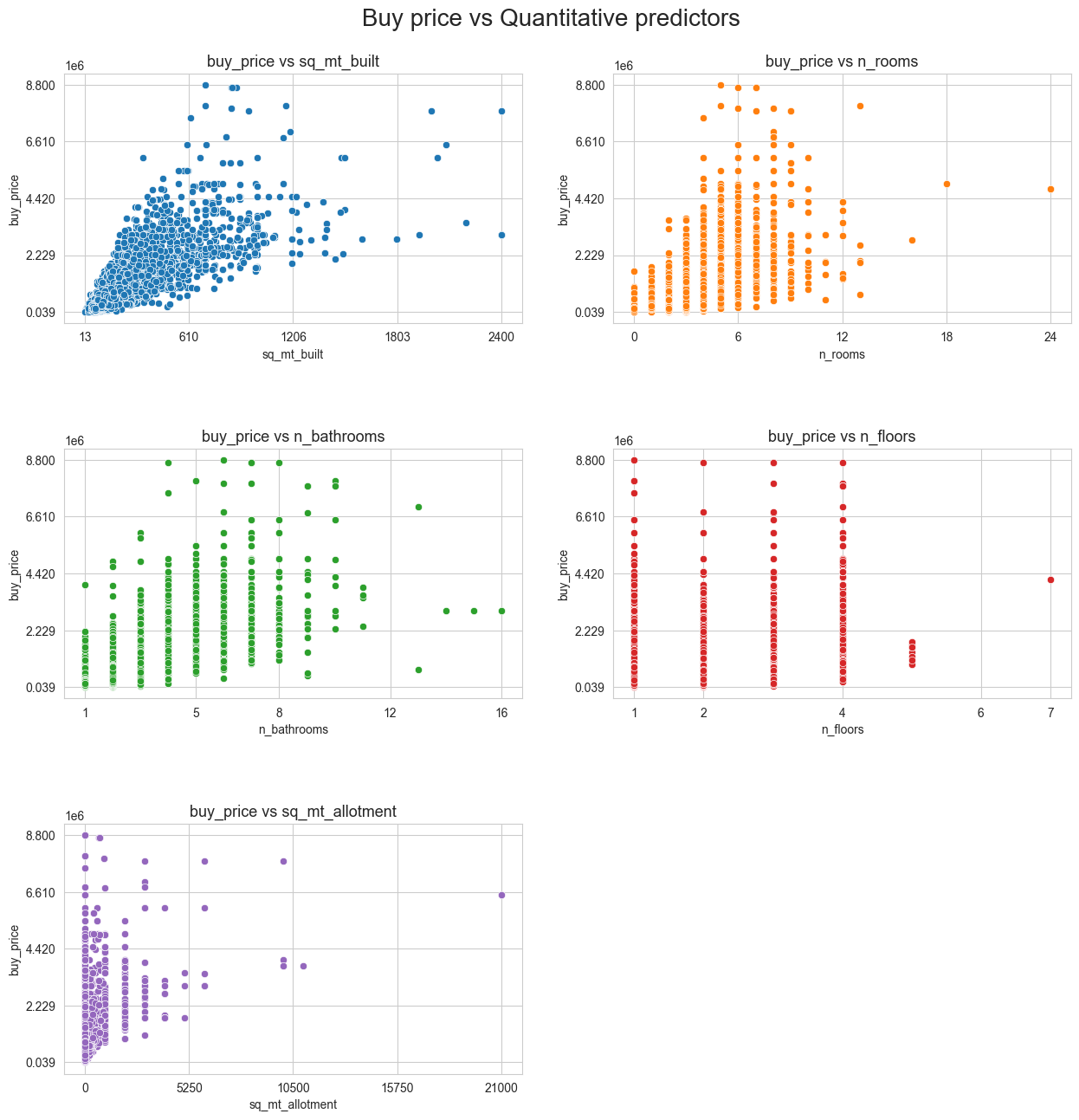

scatter_matrix(df=X_Y_train_df, n_cols=2, tittle='Buy price vs Quantitative predictors',

figsize=(15,15), response=[response], predictors=quant_predictors,

n_yticks=5, n_xticks=5, title_height=0.93, hspace=0.5, fontsize=20)

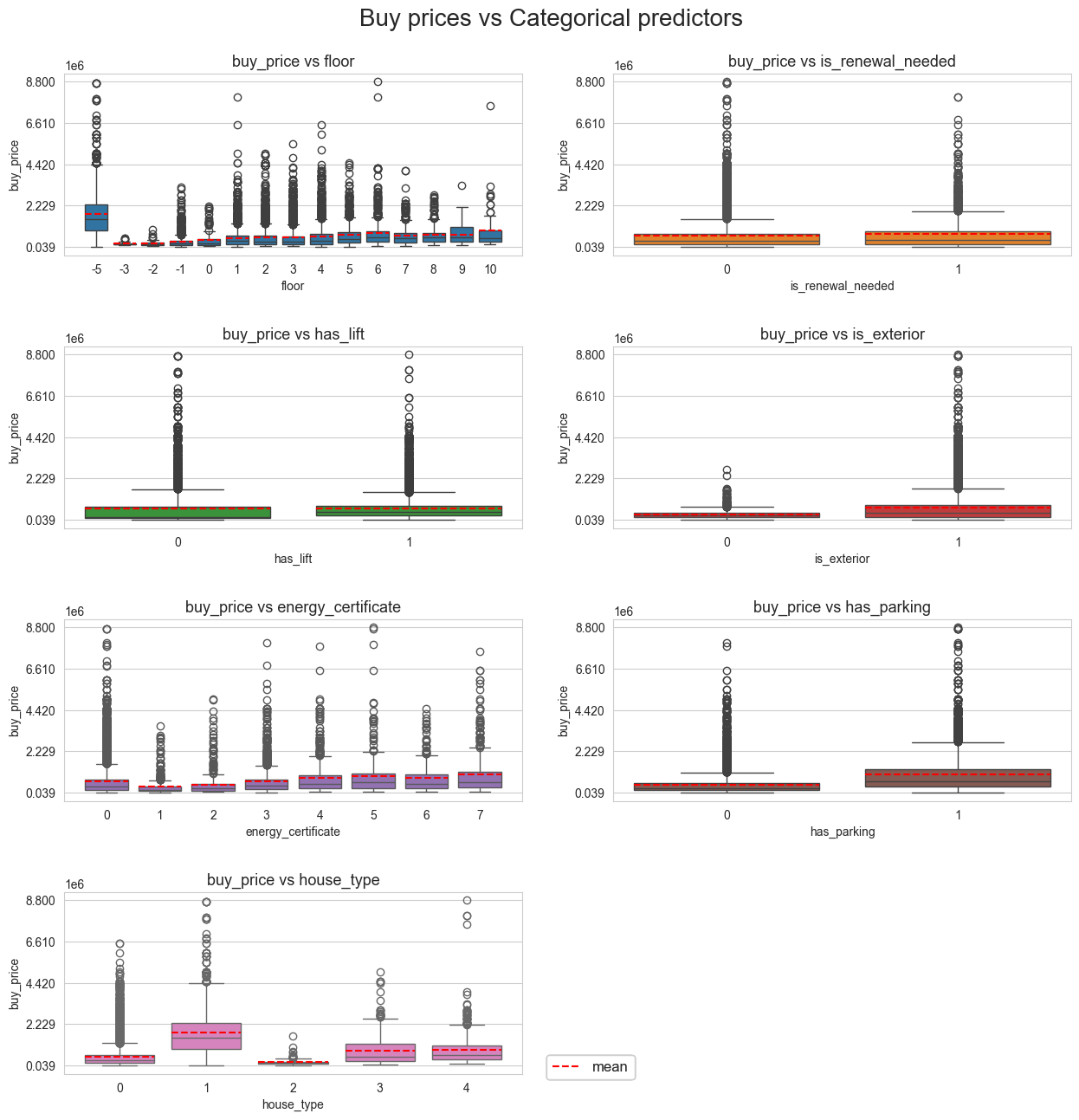

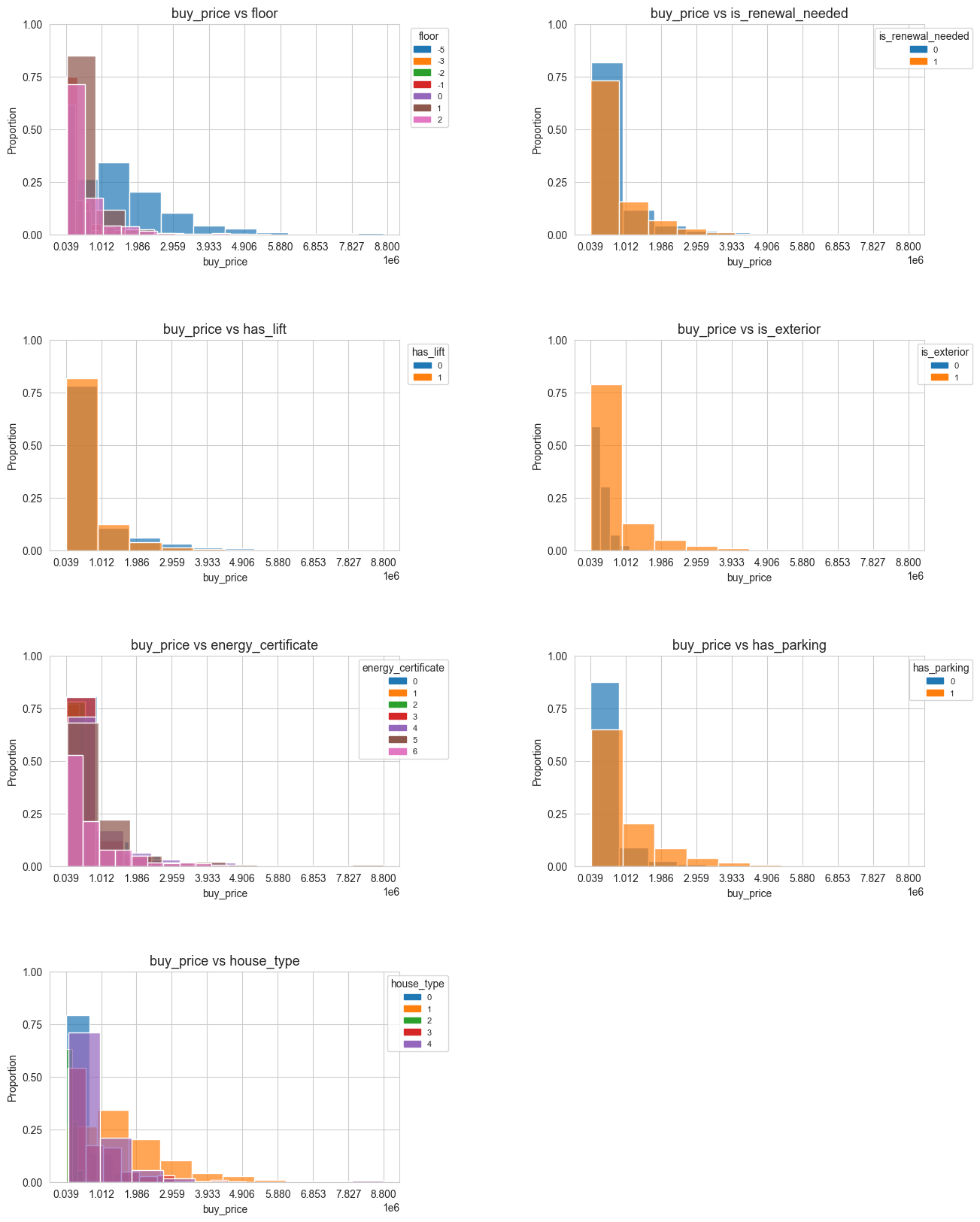

boxplot_2D_matrix(df=X_Y_train_df, n_cols=2, tittle='Buy prices vs Categorical predictors', figsize=(15,15),

response=[response], predictors=cat_predictors,

n_yticks=5, title_height=0.93, hspace=0.5, fontsize=20,

statistics=['mean'], lines_width=0.8, bbox_to_anchor=(0.53,0.1),

legend_size=12, color_stats=['red'], showfliers=True)

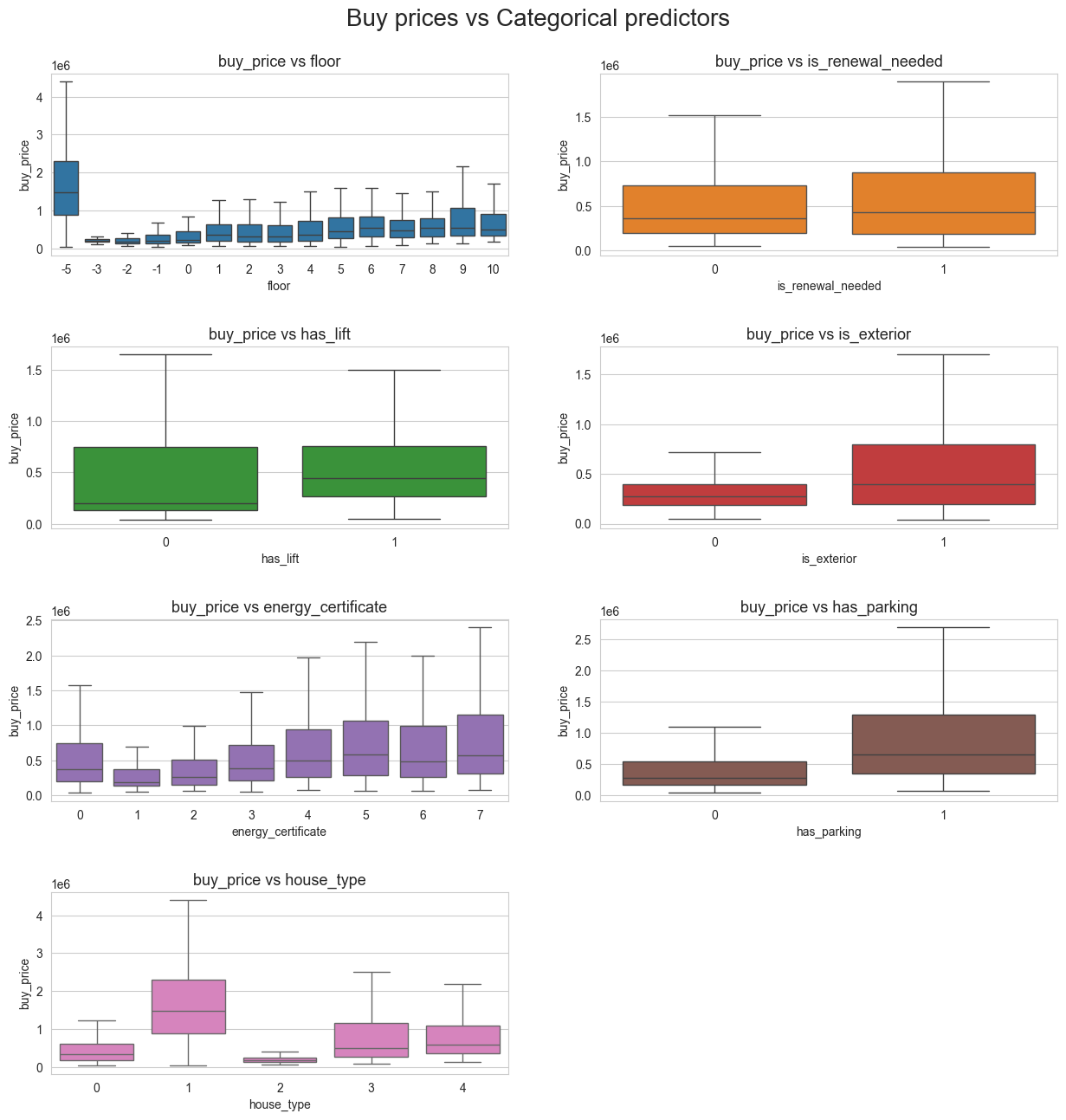

boxplot_2D_matrix(df=X_Y_train_df, n_cols=2, tittle='Buy prices vs Categorical predictors', figsize=(15,15),

response=[response], predictors=cat_predictors,

n_yticks=5, title_height=0.93, hspace=0.5, fontsize=20,

showfliers=False)

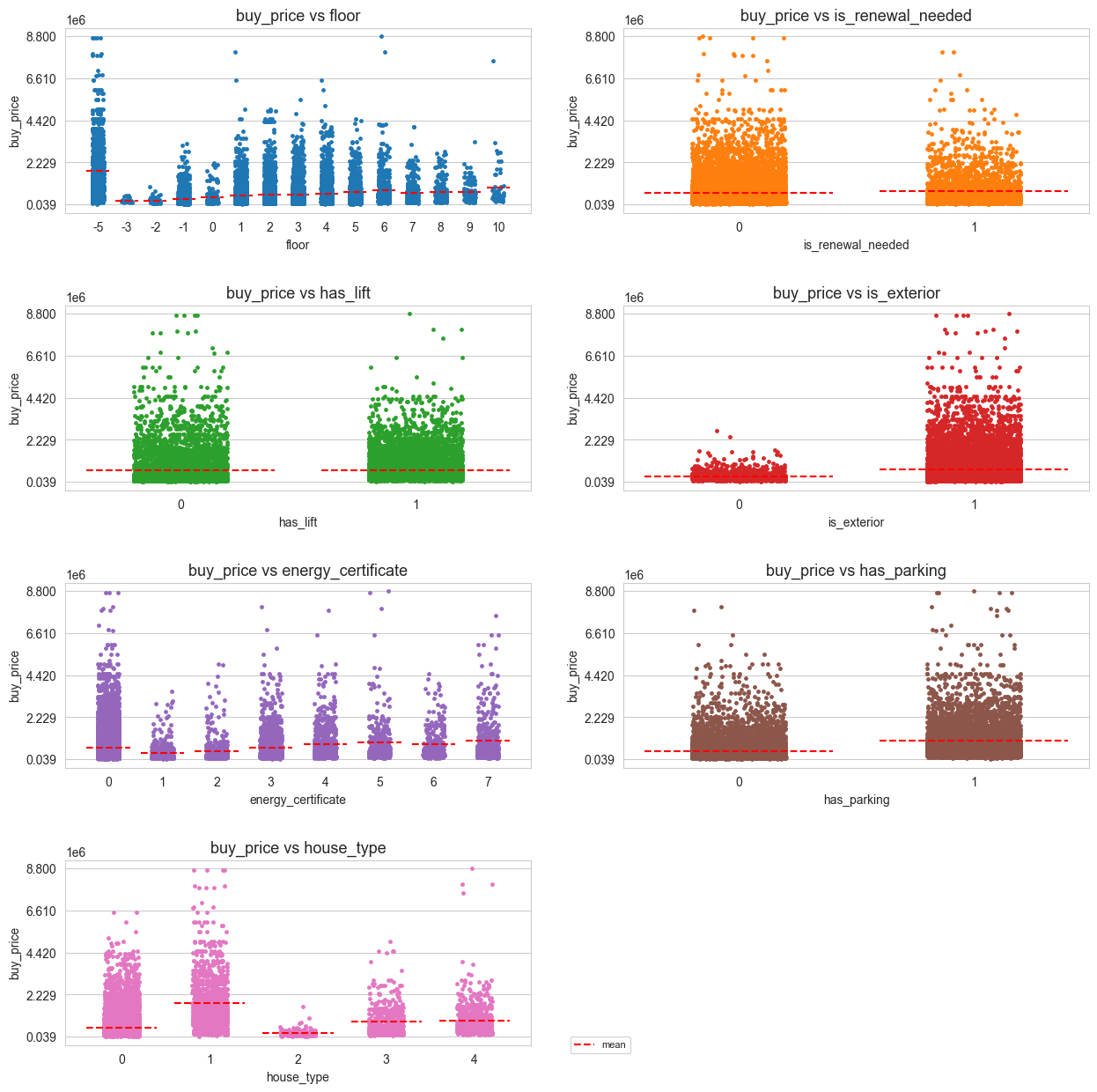

stripplot_matrix(df=X_Y_train_df, n_cols=2, tittle='', figsize=(15,15), jitter=0.2,

response=[response], predictors=cat_predictors,

n_yticks=5, title_height=0.93, hspace=0.5, fontsize=20,

statistics=['mean'], lines_width=0.8, bbox_to_anchor=(0.53, 0.1),

legend_size=8, color_stats=['red'])

histogram_2D_matrix(df=X_Y_train_df, bins=10, n_cols=2, tittle='', figsize=(15,20),

response=[response], predictors=cat_predictors,

n_yticks=5, n_xticks=10, title_height=0.93, fontsize=20,

bbox_to_anchor=(1.15, 1), wspace=0.5, hspace=0.5,

legend_size=8, transparency=0.7)

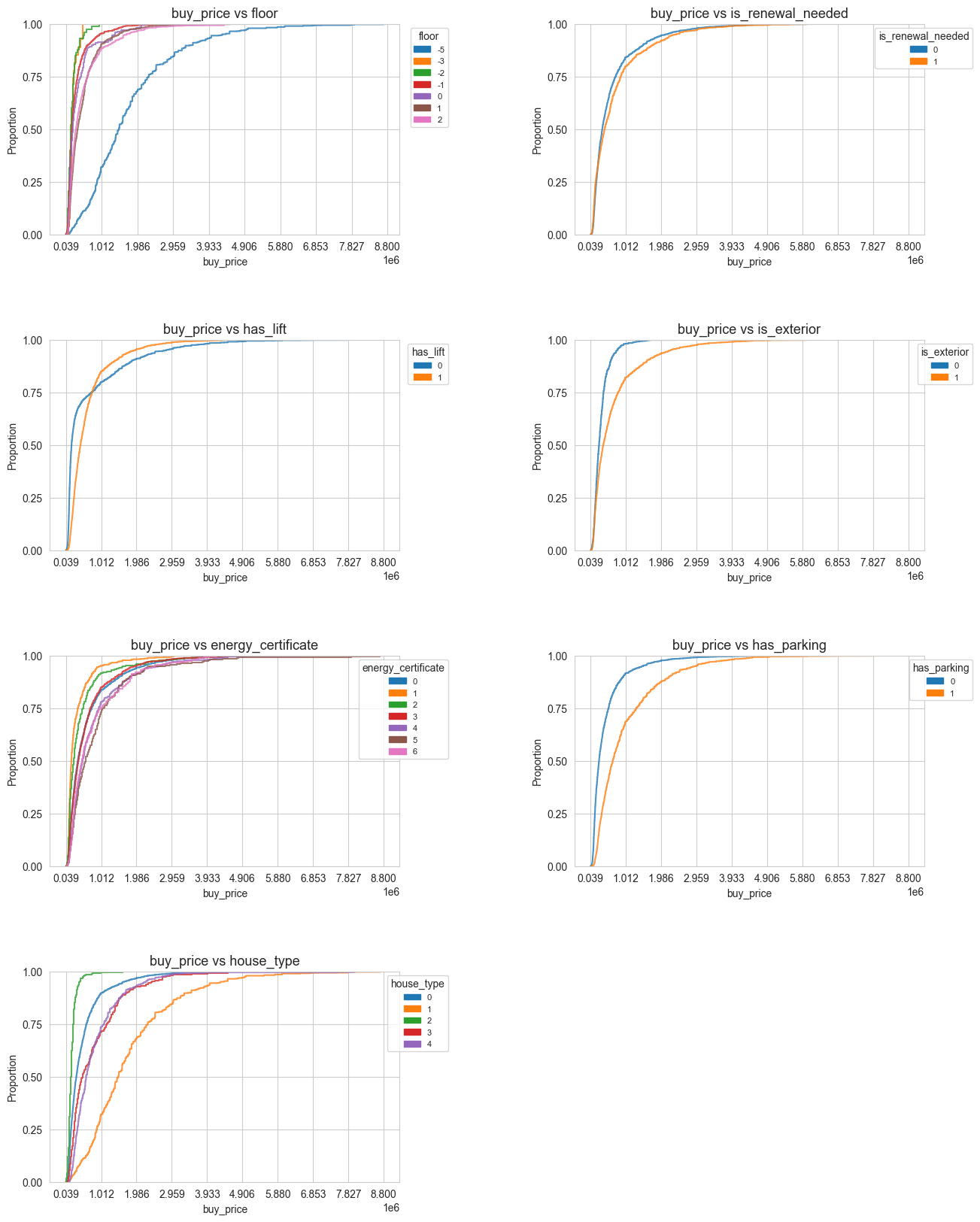

ecdf_2D_matrix(df=X_Y_train_df, n_cols=2, tittle='', figsize=(15,20),

response=[response], predictors=cat_predictors,

n_xticks=10, n_yticks=5, title_height=0.93, fontsize=20,

bbox_to_anchor=(1.15, 1), wspace=0.5, hspace=0.5,

legend_size=8, transparency=0.8)

for col in cat_predictors:

display(cross_quant_cat_summary(df=X_Y_train_df, quant_col=response, cat_col=col))

| floor | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| -5.0 | 1.7851e6 | 1.2945e6 | 39000.0 | 475200.0 | 890000.0 | 1.49e6 | 2.3e6 | 3.495e6 | 8.7e6 | 4.512 | 1.745 | 0.091837 | 0.0 |

| -3.0 | 237733.333 | 102940.106 | 115000.0 | 160000.0 | 175000.0 | 200000.0 | 250000.0 | 385000.0 | 494900.0 | 1.078 | 1.423 | 0.155172 | 0.0 |

| -2.0 | 224156.014 | 154217.86 | 74000.0 | 93900.0 | 130000.0 | 175000.0 | 259000.0 | 415000.0 | 950000.0 | 7.028 | 2.398 | 0.067879 | 0.0 |

| -1.0 | 323802.642 | 343219.37 | 42000.0 | 109000.0 | 140000.0 | 210000.0 | 359000.0 | 630000.0 | 3.2e6 | 16.575 | 3.51 | 0.105939 | 0.0 |

| 0.0 | 386954.342 | 415719.735 | 80000.0 | 124000.0 | 155000.0 | 230000.0 | 440000.0 | 790000.0 | 2.2e6 | 6.573 | 2.577 | 0.094352 | 0.0 |

| 1.0 | 515647.077 | 513707.292 | 61000.0 | 140000.0 | 199900.0 | 360000.0 | 630000.0 | 999000.0 | 8e6 | 29.949 | 3.92 | 0.083282 | 0.0 |

| 2.0 | 533162.318 | 610772.407 | 70000.0 | 130000.0 | 180000.0 | 315000.0 | 625000.0 | 1.2e6 | 5e6 | 14.534 | 3.273 | 0.100877 | 0.0 |

| 3.0 | 534463.084 | 606692.743 | 70000.0 | 130000.0 | 178000.0 | 315000.0 | 600000.0 | 1.2e6 | 5.5e6 | 10.309 | 2.878 | 0.148148 | 0.0 |

| 4.0 | 611404.858 | 714715.602 | 55000.0 | 130000.0 | 188400.0 | 365000.0 | 720000.0 | 1.375e6 | 6.5e6 | 11.715 | 3.009 | 0.091986 | 0.0 |

| 5.0 | 669036.809 | 630926.299 | 49500.0 | 175000.0 | 270000.0 | 450000.0 | 805000.0 | 1.46e6 | 4.5e6 | 6.863 | 2.344 | 0.097368 | 0.0 |

| 6.0 | 769124.274 | 809872.066 | 66000.0 | 234000.0 | 319000.0 | 550000.0 | 850000.0 | 1.74e6 | 8.8e6 | 27.77 | 4.123 | 0.046818 | 0.0 |

| 7.0 | 652867.224 | 572276.153 | 91000.0 | 215000.0 | 288000.0 | 482500.0 | 759000.0 | 1.425e6 | 4.1e6 | 8.176 | 2.485 | 0.09607 | 0.0 |

| 8.0 | 695522.421 | 552615.08 | 120000.0 | 211000.0 | 320000.0 | 540000.0 | 795000.0 | 1.5e6 | 2.8e6 | 3.154 | 1.828 | 0.007353 | 0.0 |

| 9.0 | 703932.059 | 528026.495 | 121000.0 | 203000.0 | 330000.0 | 536920.0 | 1.079e6 | 1.48e6 | 3.3e6 | 3.346 | 1.527 | 0.068493 | 0.0 |

| 10.0 | 935160.879 | 1.1675e6 | 174750.0 | 254760.0 | 321074.0 | 488250.0 | 939000.0 | 2.2797e6 | 7.525e6 | 15.856 | 3.534 | 0.082974 | 0.0 |

| is_renewal_needed | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 0.0 | 635567.578 | 759885.127 | 49000.0 | 139000.0 | 200000.0 | 365000.0 | 735000.0 | 1.495e6 | 8.8e6 | 17.864 | 3.422 | 0.095637 | 0.0 |

| 1.0 | 723705.952 | 840998.958 | 39000.0 | 126900.0 | 187000.0 | 430000.0 | 875000.0 | 1.75e6 | 8e6 | 11.796 | 2.851 | 0.087657 | 0.0 |

| has_lift | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 0.0 | 658804.012 | 1.0056e6 | 39000.0 | 109990.0 | 135000.0 | 198000.0 | 750000.0 | 1.85e6 | 8.7e6 | 11.736 | 2.986 | 0.123038 | 0.0 |

| 1.0 | 648529.815 | 644379.972 | 49000.0 | 180000.0 | 265000.0 | 445000.0 | 758000.0 | 1.4e6 | 8.8e6 | 16.46 | 3.186 | 0.088427 | 0.0 |

| is_exterior | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 0.0 | 335710.161 | 242012.879 | 52000.0 | 135000.0 | 185000.0 | 275000.0 | 399000.0 | 600000.0 | 2.7e6 | 16.453 | 3.052 | 0.06371 | 0.0 |

| 1.0 | 679795.234 | 800626.236 | 39000.0 | 135988.0 | 200000.0 | 395000.0 | 800000.0 | 1.599e6 | 8.8e6 | 15.223 | 3.174 | 0.08793 | 0.0 |

| energy_certificate | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 0.0 | 642185.792 | 753992.242 | 39000.0 | 137500.0 | 199000.0 | 369000.0 | 750000.0 | 1.5e6 | 8.7e6 | 15.746 | 3.209 | 0.102439 | 0.0 |

| 1.0 | 346668.228 | 428497.12 | 53000.0 | 113400.0 | 135000.0 | 190000.0 | 370000.0 | 740000.0 | 3.595e6 | 18.518 | 3.869 | 0.087467 | 0.0 |

| 2.0 | 475198.415 | 662838.173 | 66000.0 | 112000.0 | 148000.0 | 259000.0 | 515000.0 | 910000.0 | 5e6 | 17.032 | 3.785 | 0.109049 | 0.0 |

| 3.0 | 622401.725 | 710730.549 | 57000.0 | 139000.0 | 209000.0 | 385000.0 | 720000.0 | 1.45e6 | 8e6 | 17.811 | 3.419 | 0.096362 | 0.0 |

| 4.0 | 805999.855 | 881449.77 | 80000.0 | 169000.0 | 266000.0 | 495000.0 | 950000.0 | 1.85e6 | 7.8e6 | 11.196 | 2.823 | 0.093899 | 0.0 |

| 5.0 | 908499.322 | 1079620.2 | 70000.0 | 184000.0 | 290000.0 | 590000.0 | 1.079e6 | 1.8e6 | 8.8e6 | 19.892 | 3.787 | 0.07855 | 0.0 |

| 6.0 | 805822.84 | 815363.793 | 70000.0 | 185000.0 | 268000.0 | 482000.0 | 998000.0 | 1.85e6 | 4.5e6 | 4.193 | 2.007 | 0.081319 | 0.0 |

| 7.0 | 1.0018e6 | 1.1524e6 | 80000.0 | 175000.0 | 315000.0 | 570620.0 | 1.15e6 | 2.5e6 | 7.525e6 | 7.264 | 2.501 | 0.060302 | 0.0 |

| has_parking | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 0.0 | 461199.273 | 555863.208 | 39000.0 | 125000.0 | 161000.0 | 275000.0 | 540000.0 | 945000.0 | 8e6 | 26.332 | 4.16 | 0.076561 | 0.0 |

| 1.0 | 993549.052 | 973058.005 | 61000.0 | 235000.0 | 350000.0 | 650000.0 | 1.3e6 | 2.2e6 | 8.8e6 | 9.997 | 2.546 | 0.060584 | 0.0 |

| house_type | mean_buy_price | std_buy_price | min_buy_price | Q10_buy_price | Q25_buy_price | median_buy_price | Q75_buy_price | Q90_buy_price | max_price | kurtosis_buy_price | skew_buy_price | prop_outliers_buy_price | prop_nan_buy_price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 | f64 |

| 0.0 | 518594.384 | 569854.249 | 42000.0 | 130000.0 | 185000.0 | 330000.0 | 605000.0 | 1.06e6 | 6.5e6 | 15.006 | 3.269 | 0.08299 | 0.0 |

| 1.0 | 1.7851e6 | 1.2945e6 | 39000.0 | 475200.0 | 890000.0 | 1.49e6 | 2.3e6 | 3.495e6 | 8.7e6 | 4.512 | 1.745 | 0.052045 | 0.0 |

| 2.0 | 210529.651 | 143737.952 | 52990.0 | 99900.0 | 135000.0 | 185000.0 | 246500.0 | 330000.0 | 1.6e6 | 35.615 | 4.682 | 0.052851 | 0.0 |

| 3.0 | 810144.684 | 780032.508 | 92260.0 | 169000.0 | 270000.0 | 495000.0 | 1.175e6 | 1.75e6 | 5e6 | 5.527 | 2.054 | 0.046818 | 0.0 |

| 4.0 | 846746.026 | 826488.552 | 120000.0 | 247000.0 | 359000.0 | 598000.0 | 1.095e6 | 1.69e6 | 8.8e6 | 32.417 | 4.422 | 0.045175 | 0.0 |

Linear Regression Model#

Why Linear regression?#

The main usefulness of the linear regression model is to predict the values of a quantitative variable, called response variable, depending on the values of other, quantitative or categorical variables , called predictors.

The other important usefulness of this model is to make inference, in other words, analyze the relation between the response variable and the predictors.

Assumptions#

We have a response variable \(\mathcal{Y}\) and \(p\) predictors \(\mathcal{X} = (\mathcal{X}_1,\dots, \mathcal{X}_p).\)

We also have an \(n\) size sample of this variables: \(\hspace{0.1cm} Y\in \mathbb{R}^n, \hspace{0.2cm} X=(X_1,\dots , X_p)\in \mathbb{R}^{n\times p}\)

The model is defined as follows:

\[y_i \hspace{0.1cm} = \hspace{0.1cm} \beta_0 + x_i^\prime \cdot \beta \hspace{0.05cm}+\hspace{0.05cm} \varepsilon_i \hspace{0.1cm} = \hspace{0.1cm} \beta_0 + \beta_1 \cdot x_{i1} + \dots + \beta_p \cdot x_{ip} + \varepsilon_i\]Where:

\(x_i = (x_{i1},\dots, x_{ip})^\prime \in \mathbb{R}^p\)

\(\beta = (\beta_1, \dots, \beta_p)^\prime \in \mathbb{R}^p\)

\(\varepsilon_i\) is the residual term.

The residual term has to fulfill the following properties:

\(E[\varepsilon_i]=0\)

\(Var(\varepsilon_i)\hspace{0.05cm} = \hspace{0.05cm}\sigma^2\)

\(\varepsilon_i \sim N(0,\sigma)\)

\(cov(\varepsilon_i , \varepsilon_j)\hspace{0.05cm} = \hspace{0.05cm}0 \hspace{0.1cm} , \hspace{0.1cm} \forall i\neq j\)

Additional assumptions:

\(n \hspace{0.1cm}> \hspace{0.1cm} p+1\hspace{0.3cm}\) \((\text{nº observations} \hspace{0.05cm}> \hspace{0.05cm} \text{nº of beta coefficients})\)

\(Rg(X) \hspace{0.05cm}= \hspace{0.05cm}p+1\)

These additional assumptions are important because of the dimensionality problem.

Assumptions consequences#

\(y_i\) is a random variable because \(\varepsilon_i\) is a random variable

\(E[y_i] \hspace{0.05cm} = \hspace{0.05cm} \textbf{x}_i^T \cdot \boldsymbol{\beta}\)

\(Var(y_i) \hspace{0.05cm} = \hspace{0.05cm} \sigma^2\)

\(y_i \sim N(\hspace{0.02cm} \mathbf{x}_i^T \cdot \beta \hspace{0.03cm} , \hspace{0.1cm} \sigma^2 \hspace{0.02cm} )\)

\(cov(y_i , y_j)\hspace{0.05cm} = \hspace{0.05cm}0 \hspace{0.1cm},\hspace{0.15cm} \forall i\neq j\)

Matrix representation of the basic assumption #

\(Y \hspace{0.05cm} = \hspace{0.05cm} \beta_0 + X\cdot \beta \hspace{0.05cm} + \hspace{0.05cm}\varepsilon\)

\(\varepsilon_i \sim N(0,\sigma^2) \hspace{0.05cm} , \hspace{0.1cm} \forall \hspace{0.1cm} i=1,...,n \)

\(cov(\varepsilon_i , \varepsilon_j)\hspace{0.05cm} = \hspace{0.05cm}0 \hspace{0.05cm} , \hspace{0.1cm} \forall \hspace{0.1cm} i\neq j =1,...,n \)

Where:

\(\varepsilon =(\varepsilon_{1}, \varepsilon_{2}, ..., \varepsilon_{n})^\prime\)

Coefficient estimation#

Parameters \((\beta_0, \beta)\) are estimated by Maximum Likelihood or Ordinary Least Square (OLS). Both are equivalent under the previous assumptions.

The solution to this problem is:

Interpretation :

\(\widehat{y} = \widehat{\beta}_0 + x^\prime \cdot \widehat{\beta} \hspace{0.05cm},\hspace{0.1cm} x\in \mathbb{R}^p\hspace{0.05cm}\) is the hyperplane that minimize the euclidean distance between the values of the response variable \((y_i)\) and the projections of these values onto that hyperplane \(\hspace{0.04cm}\widehat{y}_i = \widehat{\beta}_0 + x_i^\prime \cdot \widehat{\beta} \hspace{0.04cm} .\)

We can estimate a Linear regression model in Python using statsmodels, a fantastic library to implement statistical models.

The following code is a class to perform linear regression using statsmodels implementation but with the possibility of including categorical predictors as dummy variables and interactions between the predictors.

class linear_model :

def __init__(self, X, Y):

if isinstance(X, pl.DataFrame):

X = X.to_pandas()

if isinstance(Y, pl.DataFrame):

Y = Y.to_pandas()

X = X.reset_index(drop=True)

Y = Y.reset_index(drop=True)

self.X = X

self.Y = Y

def dummies(self, X, pred_to_dummies):

X = transform_to_dummies(X, cols_to_dummies=pred_to_dummies, drop_first=True)

X = X.to_pandas()

self.pred_to_dummies = pred_to_dummies

return X

def interactions(self, X, interactions_to_add):

X_inter = pd.DataFrame()

x = interactions_to_add

if self.pred_to_dummies is not None:

X_initial = self.X # X without any changes

interactions_to_add = [(x[i][0], x[i][1]+f'_{j}')

for i in range(0, len(x))

for j in np.sort(X_initial[x[i][1]].unique())[1:]]

for quant, cat in interactions_to_add:

X_inter[f'{quant}:{cat}'] = X[quant]*X[cat]

X = pd.concat((X, X_inter), axis=1)

return X

def fit(self, pred_to_dummies=None, interactions_to_add=None):

X = self.X

self.interactions_to_add = interactions_to_add

self.pred_to_dummies = pred_to_dummies

if pred_to_dummies is not None:

X = self.dummies(X, pred_to_dummies=pred_to_dummies)

if interactions_to_add is not None:

X = self.interactions(X, interactions_to_add=interactions_to_add)

self.X_modified = X

poisson = sm.OLS(endog=self.Y, exog=X)

self.linear_fit = poisson.fit()

def predict(self, X):

pred_to_dummies = self.pred_to_dummies

interactions_to_add = self.interactions_to_add

if pred_to_dummies is not None:

X = self.dummies(X, pred_to_dummies=pred_to_dummies)

if interactions_to_add is not None:

X = self.interactions(X, interactions_to_add=interactions_to_add)

Y_hat = self.linear_fit.predict(X)

return Y_hat

Just to see how to use the class and their summary output we are going to train four full linear models. Full in the sense that hey will include all the available predictors, but we will distinguish four cases:

Full model with dummies for categorical predictors and some interactions

Full model without dummies but with interactions.

Full model with dummies but without interactions.

Full model without dummies and interactions.

# Statmodels only reads Pandas dataframes, for now.

X_train = X_train.to_pandas()

Y_train = Y_train.to_pandas()

# Full model - interactions - dummies

full_model_inter_dummies = linear_model(Y=Y_train, X=X_train)

interactions = [('n_rooms', 'is_exterior'), ('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift'), ('sq_mt_built', 'has_parking')]

full_model_inter_dummies.fit(pred_to_dummies=cat_predictors, interactions_to_add=interactions)

results_full_model_inter_dummies = full_model_inter_dummies.linear_fit.summary()

# Full model - interactions

full_model_inter = linear_model(Y=Y_train, X=X_train)

interactions = [('n_rooms', 'is_exterior'), ('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift'), ('sq_mt_built', 'has_parking')]

full_model_inter.fit(pred_to_dummies=None, interactions_to_add=interactions)

results_full_model_inter = full_model_inter.linear_fit.summary()

# Full model - dummies

full_model_dummies = linear_model(Y=Y_train, X=X_train)

full_model_dummies.fit(pred_to_dummies=cat_predictors, interactions_to_add=None)

results_full_model_dummies = full_model_dummies.linear_fit.summary()

# Full model - basic - not interactions - not dummies

full_model_basic = linear_model(Y=Y_train, X=X_train)

full_model_basic.fit(pred_to_dummies=None, interactions_to_add=None)

results_full_model_basic = full_model_basic.linear_fit.summary()

We are going to print the summaries of the respective models just to see how they look like.

print(results_full_model_inter_dummies)

OLS Regression Results

=======================================================================================

Dep. Variable: buy_price R-squared (uncentered): 0.858

Model: OLS Adj. R-squared (uncentered): 0.858

Method: Least Squares F-statistic: 2478.

Date: Fri, 29 Dec 2023 Prob (F-statistic): 0.00

Time: 10:07:47 Log-Likelihood: -2.1718e+05

No. Observations: 15217 AIC: 4.344e+05

Df Residuals: 15180 BIC: 4.347e+05

Df Model: 37

Covariance Type: nonrobust

=============================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------

sq_mt_built 1532.8474 342.962 4.469 0.000 860.601 2205.094

n_rooms -2.334e+04 1.27e+04 -1.834 0.067 -4.83e+04 1604.965

n_bathrooms 1.161e+05 4883.095 23.768 0.000 1.06e+05 1.26e+05

n_floors 2954.8637 1.15e+04 0.257 0.797 -1.96e+04 2.55e+04

sq_mt_allotment 17.1423 11.454 1.497 0.135 -5.309 39.594

floor_-2 2.16e+04 4.57e+04 0.473 0.636 -6.79e+04 1.11e+05

floor_-3 2.852e+04 7.43e+04 0.384 0.701 -1.17e+05 1.74e+05

floor_-5 1.798e+05 1.6e+04 11.269 0.000 1.49e+05 2.11e+05

floor_0 -2.145e+04 2.9e+04 -0.741 0.459 -7.82e+04 3.53e+04

floor_1 4.552e+04 1.19e+04 3.838 0.000 2.23e+04 6.88e+04

floor_10 1.921e+05 5.37e+04 3.580 0.000 8.69e+04 2.97e+05

floor_2 6.145e+04 1.2e+04 5.137 0.000 3.8e+04 8.49e+04

floor_3 7.209e+04 1.28e+04 5.646 0.000 4.71e+04 9.71e+04

floor_4 8.572e+04 1.36e+04 6.319 0.000 5.91e+04 1.12e+05

floor_5 7.016e+04 1.61e+04 4.356 0.000 3.86e+04 1.02e+05

floor_6 1.201e+05 1.87e+04 6.424 0.000 8.35e+04 1.57e+05

floor_7 5.762e+04 2.24e+04 2.574 0.010 1.37e+04 1.01e+05

floor_8 3.871e+04 2.75e+04 1.407 0.159 -1.52e+04 9.26e+04

floor_9 -3.907e+04 3.46e+04 -1.130 0.259 -1.07e+05 2.87e+04

is_renewal_needed_1 -1446.7651 8443.816 -0.171 0.864 -1.8e+04 1.51e+04

has_lift_1 -2.001e+05 1.03e+04 -19.477 0.000 -2.2e+05 -1.8e+05

is_exterior_1 -6.444e+04 1.56e+04 -4.139 0.000 -9.5e+04 -3.39e+04

energy_certificate_1 -2.954e+04 1.61e+04 -1.840 0.066 -6.1e+04 1921.923

energy_certificate_2 1.601e+04 1.84e+04 0.871 0.384 -2e+04 5.2e+04

energy_certificate_3 -1.083e+04 9581.489 -1.130 0.258 -2.96e+04 7952.322

energy_certificate_4 2.634e+04 1.44e+04 1.833 0.067 -1820.563 5.45e+04

energy_certificate_5 8.849e+04 1.96e+04 4.511 0.000 5e+04 1.27e+05

energy_certificate_6 4.643e+04 2.15e+04 2.162 0.031 4330.549 8.85e+04

energy_certificate_7 5.894e+04 1.9e+04 3.098 0.002 2.17e+04 9.62e+04

has_parking_1 -6.756e+04 1.07e+04 -6.285 0.000 -8.86e+04 -4.65e+04

house_type_1 1.798e+05 1.6e+04 11.269 0.000 1.49e+05 2.11e+05

house_type_2 914.7454 2.48e+04 0.037 0.971 -4.77e+04 4.95e+04

house_type_3 -9.499e+04 2.15e+04 -4.427 0.000 -1.37e+05 -5.29e+04

house_type_4 2.223e+04 1.61e+04 1.382 0.167 -9307.052 5.38e+04

n_rooms:is_exterior_1 -2.243e+04 1.3e+04 -1.732 0.083 -4.78e+04 2961.653

sq_mt_built:is_exterior_1 911.2754 341.102 2.672 0.008 242.674 1579.877

sq_mt_built:has_lift_1 3242.8230 65.614 49.423 0.000 3114.211 3371.435

sq_mt_built:has_parking_1 -8.3343 47.758 -0.175 0.861 -101.947 85.278

==============================================================================

Omnibus: 11702.338 Durbin-Watson: 2.014

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1216497.472

Skew: 2.995 Prob(JB): 0.00

Kurtosis: 46.391 Cond. No. 1.33e+16

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[3] The smallest eigenvalue is 2e-23. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

print(results_full_model_inter)

OLS Regression Results

=======================================================================================

Dep. Variable: buy_price R-squared (uncentered): 0.855

Model: OLS Adj. R-squared (uncentered): 0.855

Method: Least Squares F-statistic: 5595.

Date: Fri, 29 Dec 2023 Prob (F-statistic): 0.00

Time: 10:07:47 Log-Likelihood: -2.1734e+05

No. Observations: 15217 AIC: 4.347e+05

Df Residuals: 15201 BIC: 4.348e+05

Df Model: 16

Covariance Type: nonrobust

===========================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------------

sq_mt_built 1480.0192 341.947 4.328 0.000 809.762 2150.276

n_rooms -2.711e+04 1.25e+04 -2.161 0.031 -5.17e+04 -2516.047

n_bathrooms 1.239e+05 4894.994 25.311 0.000 1.14e+05 1.33e+05

n_floors 6.808e+04 8106.271 8.398 0.000 5.22e+04 8.4e+04

sq_mt_allotment 20.4074 11.486 1.777 0.076 -2.106 42.920

floor 1806.0012 1445.093 1.250 0.211 -1026.555 4638.558

is_renewal_needed 448.5235 8482.591 0.053 0.958 -1.62e+04 1.71e+04

has_lift -1.997e+05 1.02e+04 -19.554 0.000 -2.2e+05 -1.8e+05

is_exterior -1.057e+05 1.24e+04 -8.512 0.000 -1.3e+05 -8.13e+04

energy_certificate 6299.9469 1657.801 3.800 0.000 3050.459 9549.435

has_parking -4.571e+04 1.07e+04 -4.263 0.000 -6.67e+04 -2.47e+04

house_type -2961.0812 3440.179 -0.861 0.389 -9704.246 3782.083

n_rooms:is_exterior -1.23e+04 1.29e+04 -0.957 0.339 -3.75e+04 1.29e+04

sq_mt_built:is_exterior 1120.7517 339.798 3.298 0.001 454.707 1786.797

sq_mt_built:has_lift 2962.2037 63.507 46.643 0.000 2837.722 3086.686

sq_mt_built:has_parking -63.0704 48.004 -1.314 0.189 -157.163 31.023

==============================================================================

Omnibus: 11375.312 Durbin-Watson: 2.012

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1245548.674

Skew: 2.840 Prob(JB): 0.00

Kurtosis: 46.957 Cond. No. 2.81e+03

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[3] The condition number is large, 2.81e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

print(results_full_model_dummies)

OLS Regression Results

=======================================================================================

Dep. Variable: buy_price R-squared (uncentered): 0.834

Model: OLS Adj. R-squared (uncentered): 0.834

Method: Least Squares F-statistic: 2317.

Date: Fri, 29 Dec 2023 Prob (F-statistic): 0.00

Time: 10:07:47 Log-Likelihood: -2.1835e+05

No. Observations: 15217 AIC: 4.368e+05

Df Residuals: 15184 BIC: 4.370e+05

Df Model: 33

Covariance Type: nonrobust

========================================================================================

coef std err t P>|t| [0.025 0.975]

----------------------------------------------------------------------------------------

sq_mt_built 3335.6205 46.524 71.697 0.000 3244.428 3426.812

n_rooms -1.104e+04 3651.373 -3.024 0.003 -1.82e+04 -3883.486

n_bathrooms 1.745e+05 5109.825 34.159 0.000 1.65e+05 1.85e+05

n_floors -1.873e+05 1.05e+04 -17.917 0.000 -2.08e+05 -1.67e+05

sq_mt_allotment -203.9127 11.375 -17.927 0.000 -226.208 -181.617

floor_-2 -1.672e+04 4.92e+04 -0.340 0.734 -1.13e+05 7.97e+04

floor_-3 -2.159e+04 8e+04 -0.270 0.787 -1.78e+05 1.35e+05

floor_-5 9.356e+04 1.64e+04 5.716 0.000 6.15e+04 1.26e+05

floor_0 -4.151e+04 3.1e+04 -1.338 0.181 -1.02e+05 1.93e+04

floor_1 1.507e+04 1.24e+04 1.219 0.223 -9170.640 3.93e+04

floor_10 1.517e+05 5.78e+04 2.622 0.009 3.83e+04 2.65e+05

floor_2 3.915e+04 1.24e+04 3.145 0.002 1.48e+04 6.36e+04

floor_3 5.149e+04 1.33e+04 3.858 0.000 2.53e+04 7.77e+04

floor_4 7.532e+04 1.43e+04 5.280 0.000 4.74e+04 1.03e+05

floor_5 5.628e+04 1.71e+04 3.296 0.001 2.28e+04 8.97e+04

floor_6 1.078e+05 1.99e+04 5.414 0.000 6.87e+04 1.47e+05

floor_7 3.238e+04 2.4e+04 1.350 0.177 -1.46e+04 7.94e+04

floor_8 1.446e+04 2.96e+04 0.488 0.625 -4.36e+04 7.25e+04

floor_9 -3.121e+04 3.73e+04 -0.838 0.402 -1.04e+05 4.18e+04

is_renewal_needed_1 2.865e+04 9052.496 3.165 0.002 1.09e+04 4.64e+04

has_lift_1 8.137e+04 8818.001 9.228 0.000 6.41e+04 9.87e+04

is_exterior_1 -6.605e+04 1.11e+04 -5.964 0.000 -8.78e+04 -4.43e+04

energy_certificate_1 -4.099e+04 1.73e+04 -2.369 0.018 -7.49e+04 -7078.883

energy_certificate_2 -9636.5864 1.98e+04 -0.486 0.627 -4.85e+04 2.92e+04

energy_certificate_3 -1.93e+04 1.03e+04 -1.867 0.062 -3.95e+04 957.103

energy_certificate_4 2.805e+04 1.55e+04 1.809 0.070 -2343.800 5.85e+04

energy_certificate_5 1.01e+05 2.12e+04 4.767 0.000 5.95e+04 1.42e+05

energy_certificate_6 2.95e+04 2.32e+04 1.273 0.203 -1.59e+04 7.49e+04

energy_certificate_7 5.37e+04 2.05e+04 2.619 0.009 1.35e+04 9.39e+04

has_parking_1 -2.764e+04 8066.556 -3.427 0.001 -4.35e+04 -1.18e+04

house_type_1 9.356e+04 1.64e+04 5.716 0.000 6.15e+04 1.26e+05

house_type_2 5826.3125 2.66e+04 0.219 0.827 -4.63e+04 5.79e+04

house_type_3 1.437e+05 2.22e+04 6.465 0.000 1e+05 1.87e+05

house_type_4 7.542e+04 1.73e+04 4.351 0.000 4.14e+04 1.09e+05

==============================================================================

Omnibus: 8988.079 Durbin-Watson: 2.022

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1125984.333

Skew: 1.880 Prob(JB): 0.00

Kurtosis: 44.973 Cond. No. 1.27e+16

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[3] The smallest eigenvalue is 1.72e-23. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

print(results_full_model_basic)

OLS Regression Results

=======================================================================================

Dep. Variable: buy_price R-squared (uncentered): 0.833

Model: OLS Adj. R-squared (uncentered): 0.833

Method: Least Squares F-statistic: 6323.

Date: Fri, 29 Dec 2023 Prob (F-statistic): 0.00

Time: 10:07:47 Log-Likelihood: -2.1841e+05

No. Observations: 15217 AIC: 4.368e+05

Df Residuals: 15205 BIC: 4.369e+05

Df Model: 12

Covariance Type: nonrobust

======================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------

sq_mt_built 3361.2021 46.165 72.808 0.000 3270.713 3451.691

n_rooms -1.082e+04 3522.682 -3.073 0.002 -1.77e+04 -3919.647

n_bathrooms 1.762e+05 5103.800 34.515 0.000 1.66e+05 1.86e+05

n_floors -1.394e+05 6846.789 -20.359 0.000 -1.53e+05 -1.26e+05

sq_mt_allotment -195.4226 11.286 -17.316 0.000 -217.544 -173.301

floor 5199.6852 1494.271 3.480 0.001 2270.735 8128.636

is_renewal_needed 2.364e+04 9034.689 2.616 0.009 5928.776 4.13e+04

has_lift 6.459e+04 8148.929 7.926 0.000 4.86e+04 8.06e+04

is_exterior -8.815e+04 9927.824 -8.879 0.000 -1.08e+05 -6.87e+04

energy_certificate 5251.0132 1771.320 2.964 0.003 1779.014 8723.012

has_parking -1.978e+04 7990.224 -2.476 0.013 -3.54e+04 -4118.021

house_type 2.391e+04 3626.919 6.592 0.000 1.68e+04 3.1e+04

==============================================================================

Omnibus: 8971.290 Durbin-Watson: 2.020

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1170728.967

Skew: 1.863 Prob(JB): 0.00

Kurtosis: 45.809 Cond. No. 1.42e+03

==============================================================================

Notes:

[1] R² is computed without centering (uncentered) since the model does not contain a constant.

[2] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[3] The condition number is large, 1.42e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

Standard deviation of coefficients#

The precision of beta coefficients estimations is given by the standard deviation of their estimators:

where:

\(q_{jj}\hspace{0.05cm} = diag\left( (X^T \cdot X)^{-1} \right)[j+1]\hspace{0.05cm}\) is the \(j+1\) element of the principal diagonal of the matrix \((X^T \cdot X)^{-1}\) \(\hspace{0.01cm} , \hspace{0.05cm}\) for \(\small{j=0,1,\dots,p}\) .

To estimate \(sd(\widehat{\beta}_j)\) we need to estimate \(\sigma^2\), i.e, the variance of the error term \(\varepsilon_i\).

We can estimate it as follows:

where:

\(RSS = \sum_{i=1}^{n} \hspace{0.05cm}\widehat{\varepsilon}_i^2\) is the residual sum of squares.

\(\widehat{\varepsilon}_i = y_i - \widehat{y}_i\) is the estimation of the \(i\)-th residual term.

Then, we have the following estimation for the standard deviation of the coefficients:

Why is the variance of the coefficient estimators important?

The standard deviation of a coefficient estimator indicates how much the estimation of that coefficient varies, in mean, when the model is trained with many different samples.

Suppose many samples are obtained, and with each of them a linear regression model is trained. Then, we get many estimations of the model coefficient \(\widehat{\beta}_j\), one with each sample.

Then, \(s_d(\widehat{\beta}_j)\) indicates how much \(\widehat{\beta}_j\) varies from one sample to another, in mean.

Interpretation:

If the standard deviation is high, this indicates that will be obtained big differences when \(\beta_j\) is estimate with \(\widehat{\beta}_j\) depending on the sample that is used for estimate it, that means estimator \(\widehat{\beta}_j\) is imprecise, because it will be much dispersion of the values of \(\widehat{\beta}_j\) respect to the mean.

On the contrary, if the standard deviation is low, this indicates that will be obtained small differences when \(\beta_j\) is estimate with \(\widehat{\beta}_j\) depending on the sample that is used for estimate it, that means estimator \(\widehat{\beta}_j\) is precise, because it will be little dispersion of the values of \(\widehat{\beta}_j\) respect to the mean.

In addition, \(\widehat{s_d}(\widehat{\beta}_j)\) allows to define a confidence interval for \(\widehat{\beta}_j\) estimator .

We can obtain the estimation fo the standard deviation of coefficient estimators with our class as follows:

full_model_inter_dummies.linear_fit.bse

sq_mt_built 342.961695

n_rooms 12727.596343

n_bathrooms 4883.094974

n_floors 11493.166017

sq_mt_allotment 11.454317

floor_-2 45685.141817

floor_-3 74314.873388

floor_-5 15959.232517

floor_0 28964.054054

floor_1 11861.824556

floor_10 53666.317778

floor_2 11961.359039

floor_3 12769.649023

floor_4 13566.003037

floor_5 16106.923393

floor_6 18701.565813

floor_7 22382.217113

floor_8 27512.954519

floor_9 34577.619792

is_renewal_needed_1 8443.816143

has_lift_1 10273.791241

is_exterior_1 15569.325847

energy_certificate_1 16050.032312

energy_certificate_2 18377.709130

energy_certificate_3 9581.488722

energy_certificate_4 14368.369556

energy_certificate_5 19618.537772

energy_certificate_6 21476.579454

energy_certificate_7 19023.827742

has_parking_1 10748.365169

house_type_1 15959.232517

house_type_2 24788.864438

house_type_3 21458.713817

house_type_4 16091.495675

n_rooms:is_exterior_1 12956.445872

sq_mt_built:is_exterior_1 341.102462

sq_mt_built:has_lift_1 65.614214

sq_mt_built:has_parking_1 47.758490

dtype: float64

Confidence intervals for coefficients#

Confidence intervals for beta coefficients at a level \(1-\alpha\) can be defined as follows:

Observation:

The smaller \(\widehat{s_d}(\widehat{\beta}_j)\), the smaller \(CI(\beta_j)\).

Using our class these confidence intervals can be obtained as follows:

betas_CI = full_model_inter_dummies.linear_fit.conf_int(alpha=0.05)

betas_CI.columns = ['2.5%', '97.5%']

betas_CI

| 2.5% | 97.5% | |

|---|---|---|

| sq_mt_built | 860.601179 | 2205.093522 |

| n_rooms | -48290.274169 | 1604.965066 |

| n_bathrooms | 106488.712368 | 125631.619276 |

| n_floors | -19573.123999 | 25482.851420 |

| sq_mt_allotment | -5.309497 | 39.594179 |

| floor_-2 | -67947.157168 | 111149.588124 |

| floor_-3 | -117142.811317 | 174189.368494 |

| floor_-5 | 148561.896433 | 211125.926824 |

| floor_0 | -78223.279453 | 35322.779618 |

| floor_1 | 22269.505846 | 68770.711419 |

| floor_10 | 86907.704353 | 297292.579248 |

| floor_2 | 38001.357637 | 84892.762324 |

| floor_3 | 47061.751438 | 97121.847295 |

| floor_4 | 59132.930780 | 112314.925930 |

| floor_5 | 38586.221564 | 101729.235716 |

| floor_6 | 83479.099833 | 156793.736404 |

| floor_7 | 13747.950497 | 101491.625530 |

| floor_8 | -15220.609435 | 92636.790406 |

| floor_9 | -106845.010601 | 28707.576483 |

| is_renewal_needed_1 | -17997.660287 | 15104.130116 |

| has_lift_1 | -220240.977098 | -179965.244118 |

| is_exterior_1 | -94959.788264 | -33924.285808 |

| energy_certificate_1 | -60998.064103 | 1921.923328 |

| energy_certificate_2 | -20011.903303 | 52033.137167 |

| energy_certificate_3 | -29609.418365 | 7952.322211 |

| energy_certificate_4 | -1820.562564 | 54506.902347 |

| energy_certificate_5 | 50037.593213 | 126946.980438 |

| energy_certificate_6 | 4330.549406 | 88523.906965 |

| energy_certificate_7 | 21652.184603 | 96230.165451 |

| has_parking_1 | -88623.480438 | -46487.303504 |

| house_type_1 | 148561.896433 | 211125.926824 |

| house_type_2 | -47674.410344 | 49503.901108 |

| house_type_3 | -137055.965536 | -52932.645570 |

| house_type_4 | -9307.052383 | 53775.481406 |

| n_rooms:is_exterior_1 | -47830.731598 | 2961.652840 |

| sq_mt_built:is_exterior_1 | 242.673582 | 1579.877285 |

| sq_mt_built:has_lift_1 | 3114.211238 | 3371.434739 |

| sq_mt_built:has_parking_1 | -101.946727 | 85.278040 |

Goodness of fit#

R-square#

The R-square is a measure of the goodness of fit of the linear regression model to the training data.

Where:

Total Sum Squares

Residual Sum Squares

Regression Sum Squares

It can be proved that:

where:

\(TSS \hspace{0.05cm}\) is the total variance of the response variable \(Y\)

\(RegSS \hspace{0.05cm}\) is the variance of the response variable \(Y\) explained by the model using \(X\)

\(RSS \hspace{0.05cm}\) is the variance of the response variable \(Y\) not explained by the model using \(X\)

Properties:

\(R^2\) is the total variance of the response explaining by the linear regression model by mean of the predictors.

\(R^2 \in \left[ 0 , 1 \right]\)

For this reason, \(\hspace{0.01cm}R^2\hspace{0.01cm}\) is used as a measure of how well the model fits the response variable.

Interpretation:

The \(\hspace{0.01cm}R^2\hspace{0.01cm}\) interpretation is the following:

If \(\hspace{0.01cm}R^2\hspace{0.01cm}\) is close to \(1\), this means that the model is fitting well the response data.

If \(\hspace{0.01cm}R^2\hspace{0.01cm}\) is close to \(0\), this means that the model is fitting badly the response data.

We can obtain it using our class as follows:

full_model_inter_dummies.linear_fit.rsquared

0.8579358772571637

Adjusted R-square#

The \(R^2\) has some problems:

\(\hspace{0.1cm} R^2\) always increase when increase the number of predictors, although they are not significative.

It´s possible estimate two models with the same prediction power but with different \(\hspace{0.1cm}R^2\)

For avoid the disadvantages of \(\hspace{0.1cm}R^2\hspace{0.1cm}\) was created the adjusted \(\hspace{0.1cm}R^2\hspace{0.1cm}\) , denoted as \(\widehat{R^2}\), and defined as:

This metric doesn’t grow when including irrelevant predictors, because if \(\hspace{0.1cm} RSS\hspace{0.1cm}\) is small because of \(\hspace{0.1cm}p\hspace{0.1cm}\) is large, then \(\hspace{0.1cm}1/(n-p-1)\hspace{0.1cm}\) will be large compensating the \(\hspace{0.01cm}RSS\hspace{0.01cm}\) value

We can obtain it using our class as follows:

full_model_inter_dummies.linear_fit.rsquared_adj

0.8575896076562753

Global Significance Test (ANOVA)#

The test of model global significance is also called ANOVA test, and is defined by the following hypothesis :

Statistic:

The test statistic for the ANOVA test is the following:

Decision Rule:

Based on test statistic:

\[ \text{Reject} \hspace{0.05cm} H_0 \hspace{0.1cm} \Leftrightarrow \hspace{0.1cm} F_{exp|H_0} > F_{\alpha}^{\hspace{0.1cm}p,\hspace{0.05cm} n-p-1} \]where:

\[ P(F_{\hspace{0.05cm}p,\hspace{0.05cm} n-p-1} > F_{\alpha}^{\hspace{0.1cm}p,\hspace{0.05cm} n-p-1} ) = \alpha \]Based on p-value:

\[ \text{Reject} \hspace{0.05cm} H_0 \hspace{0.1cm} \Leftrightarrow \hspace{0.1cm} p\text{-value} < \alpha \]where:

\[ p\text{-value} = P(F_{\hspace{0.05cm}p,\hspace{0.05cm} n-p-1} \geq F_{exp|H_0} ) \]

We can obtain the observed value of the statistic and the pvalue of the test from our class as follows:

full_model_inter_dummies.linear_fit.fvalue

2477.6528897026333

full_model_inter_dummies.linear_fit.f_pvalue

0.0

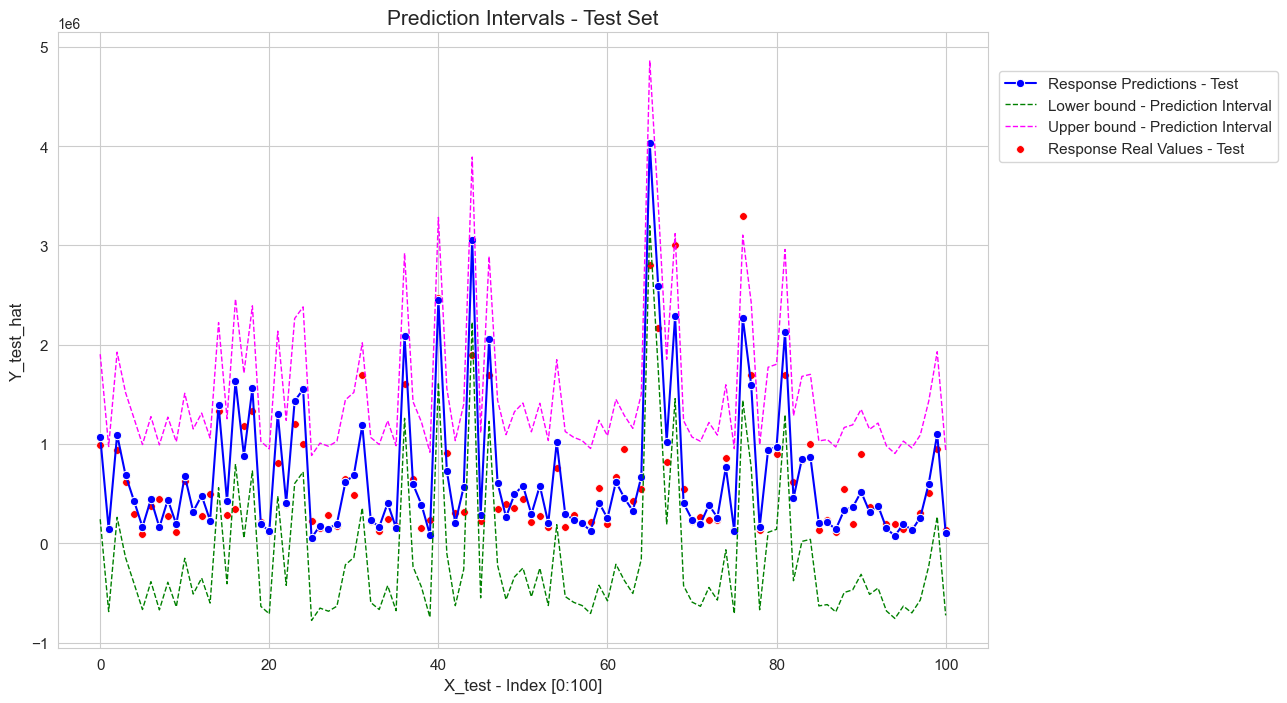

Prediction#

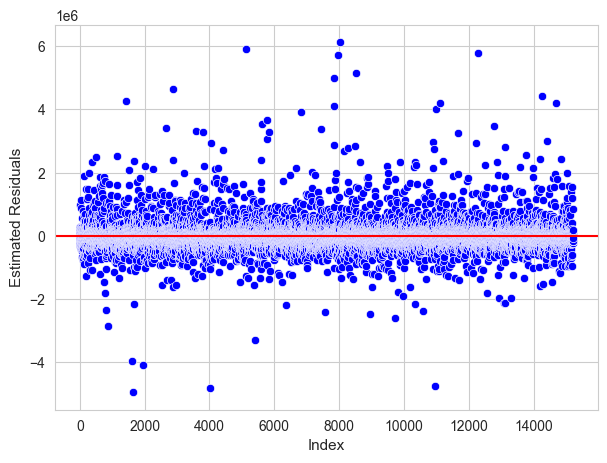

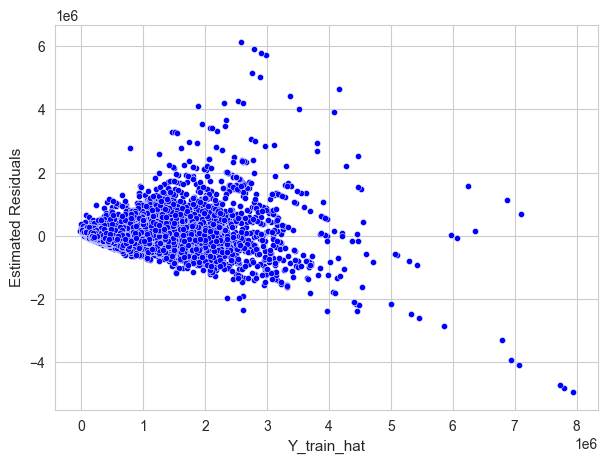

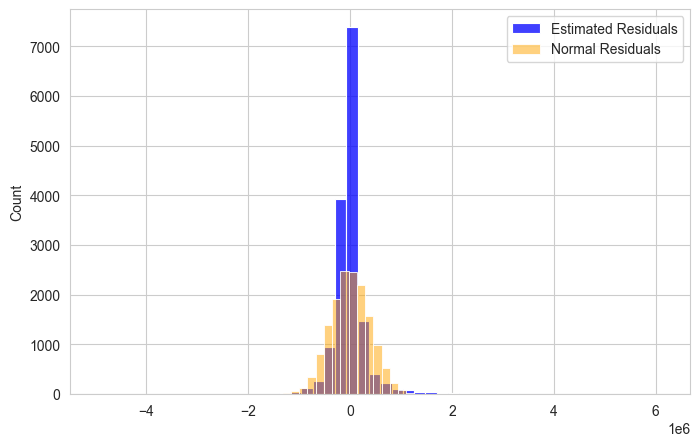

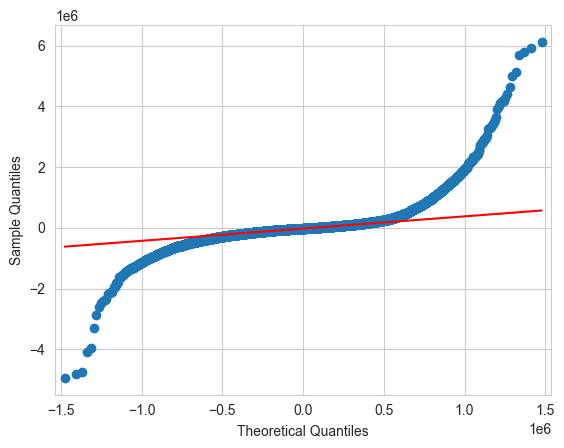

Once we have estimated the model parameters we can make predictions on the response using data of the predictors.

The prediction of the response for individuals with the value \(x_i \in \mathbb{R}^p\) for the predictors is:

# Full model - interactions - dummies

full_model_inter_dummies = linear_model(Y=Y_train, X=X_train)

interactions = [('n_rooms', 'is_exterior'), ('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift'), ('sq_mt_built', 'has_parking')]

full_model_inter_dummies.fit(pred_to_dummies=cat_predictors, interactions_to_add=interactions)

# Computing predictions

Y_train_hat = full_model_inter_dummies.predict(X_train)

# Computing RMSE

np.sqrt(np.mean((Y_train_hat - Y_train.to_numpy())**2))

381995.050363493

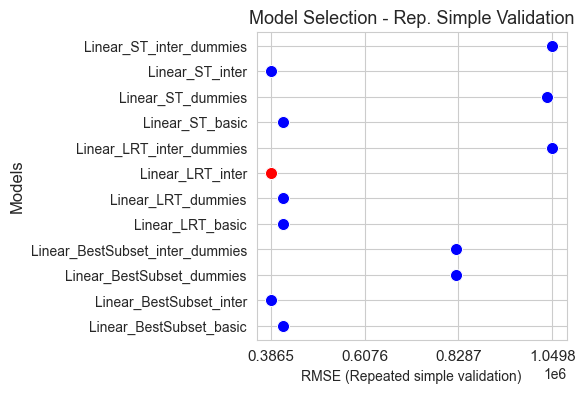

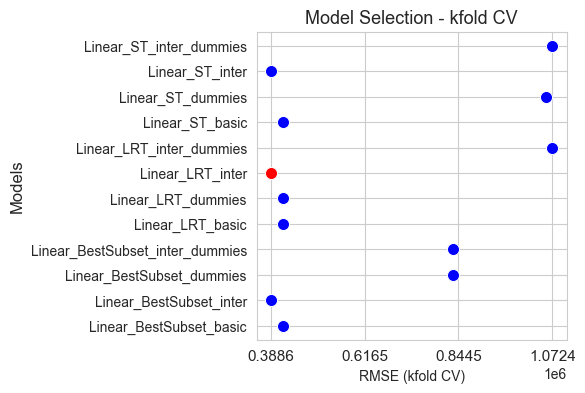

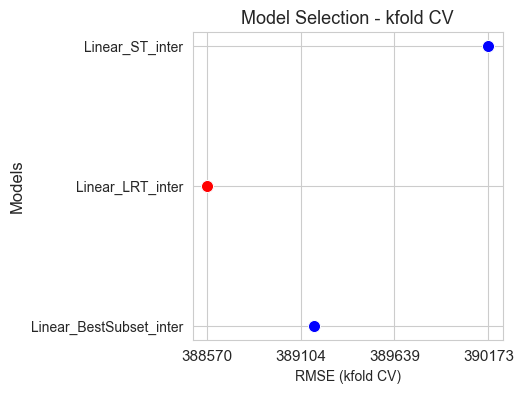

Predictors Selection#

In this section we are going to explore several methods to select predictors.

Given a data set with \(p\) predictors, the number of possible linear regression model that can be trained with a subset (all included) of them is:

Where:

is the number of possible combinations of \(k\) objects selected from a set of \(p\) objects, without repetition and where the order does not matter, is given by the binomial coefficient:

def binom(p,k) :

return factorial(p) / (factorial(k)*factorial(p-k))

p = X_train.shape[1]

np.sum([binom(p,k) for k in range(1,p+1)])

4095.0

In this case we can train 4095 different linear regression model with our data set, that has \(p=12\) predictors.

So, we are interested in a way to select the “best” combination of predictors. There is no definitive method, so, we will see several options.

Significance Test#

The (individual) significance test (ST) for the predictor \(\mathcal{X}_j\) consists in testing the following hypothesis

\begin{cases} H_0 : \beta_j = 0 \ H_1 : \beta_j \neq 0 \end{cases}

Statistic:

p-value:

Decision rule based in p-value:

If \(\hspace{0.1cm}\text{p-value} < \alpha \hspace{0.1cm} \Rightarrow\hspace{0.1cm}\) Reject \(H_0 \hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) predictor \(\mathcal{X}_j\) is significative to explain the response.

If \(\hspace{0.1cm}\text{p-value} \geq \alpha \hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) Not Reject \(H_0 \hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) predictor \(\mathcal{X}_j\) is not significative to explain the response.

Decision rule basede in confidence intervals:

This test can be performed with the confidence intervals of the coefficients as follows:

If \(\hspace{0.1cm}0\in CI(\beta_j)\hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) Not reject \(H_0\)

If \(\hspace{0.1cm}0\in CI(\beta_j)\hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) Reject \(H_0\)

Where:

\(P\left(t_{n-p-1} > t^{n-p-1}_{\alpha/2} \right) = \alpha/2\)

The following function allow us to extract the significant predictors of a given linear regression model according to the above test.

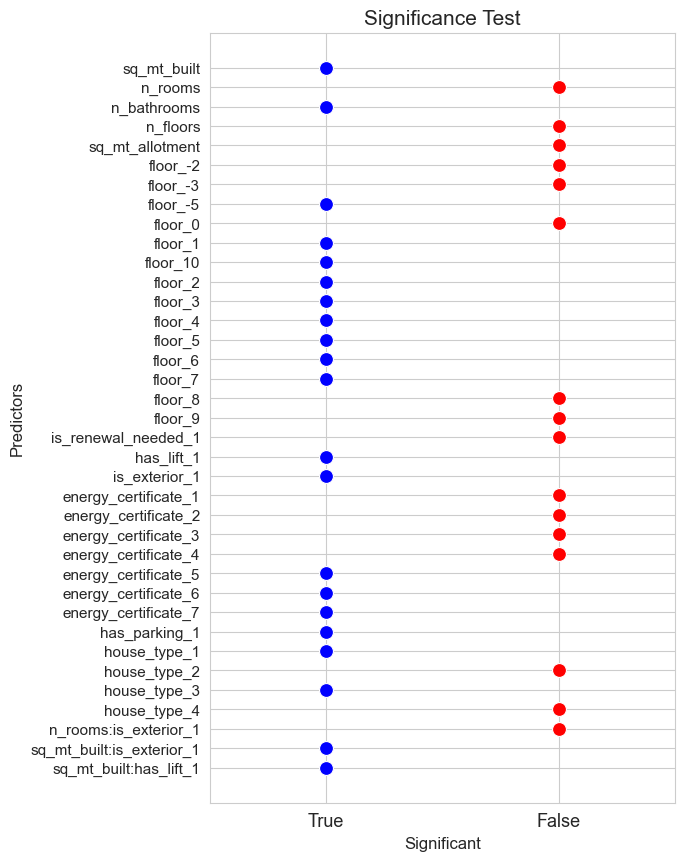

def significant_test(model, alpha=0.05, figsize=(5, 6)) :

pvalues = model.linear_fit.pvalues.values

pvalues = pvalues[0:len(pvalues)-1]

predictors = model.linear_fit.pvalues.index.to_numpy()

predictors = predictors[0:len(predictors)-1]

significant_results = pvalues < alpha

significant_predictors = predictors[significant_results==True]

not_significant_predictors = predictors[significant_results==False]

significant_results_str = np.array([str(x) for x in significant_results])

plt.figure(figsize=figsize)

ax = sns.scatterplot(x=significant_results_str, y=predictors, color='red', s=100)

ax = sns.scatterplot(x=significant_results_str[significant_results==True],

y=predictors[significant_results==True], color='blue', s=100)

plt.title('Significance Test', size=15)

ax.set_ylabel('Predictors', size=12)

ax.set_xlabel('Significant', size=12)

plt.xticks(fontsize=13)

plt.yticks(fontsize=11)

ax.set_xlim(-0.5, 1.5)

plt.show()

return significant_predictors, not_significant_predictors

The idea is to applied this method to the full model (the one that include all the predictors) to identify which of them are not significative (according to the above test), and therefore we will select one combination of predictors, the significative one.

Since we have four full models, as we explained before, we will apply the test to all of them, and we will obtain a “final” set of predictors in each case.

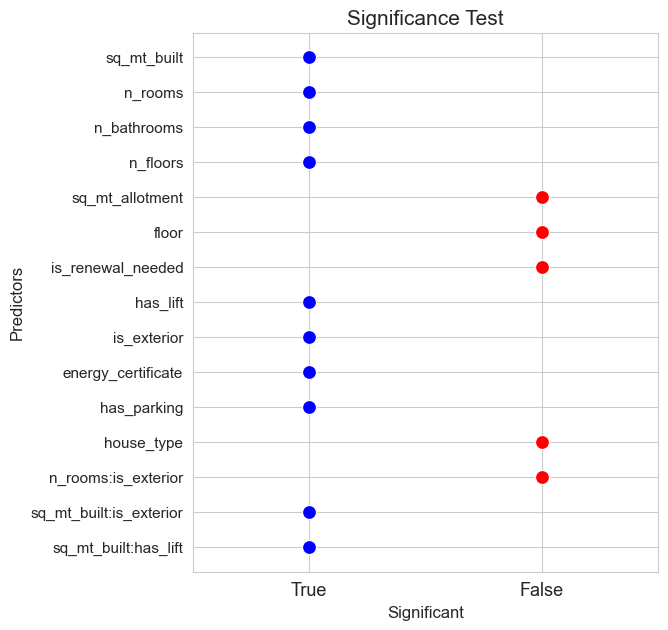

# Full model - interactions - dummies

significant_pred_model_inter_dummies_ST, not_significant_pred_model_inter_dummies_ST = significant_test(model=full_model_inter_dummies, alpha=0.05, figsize=(6,10))

Given a categorical predictor, if at least one dummy is significative, we consider the predictor significative. And the same for the interactions.

def recognition(initial_list):

output_list = []

for x in initial_list :

try :

int(x.split('_')[len(x.split('_'))-1])

list_strings = x.split('_')[:len(x.split('_'))-1]

output_list.append('_'.join(list_strings))

except:

output_list.append(x)

output_list = list(set(output_list))

return np.array(output_list)

predictors_selected, interactions_selected, pred_to_dummies = {}, {}, {}

significant_pred_model_inter_dummies_ST = recognition(significant_pred_model_inter_dummies_ST)

not_significant = recognition(not_significant_pred_model_inter_dummies_ST)

not_significant_pred_model_inter_dummies_ST = np.array([x for x in not_significant if x not in significant_pred_model_inter_dummies_ST])

predictors_selected['ST_inter_dummies'] = [x for x in significant_pred_model_inter_dummies_ST if ':' not in x]

interactions_selected['ST_inter_dummies'] = [(x.split(':')[0], x.split(':')[1]) for x in significant_pred_model_inter_dummies_ST if ':' in x]

pred_to_dummies['ST_inter_dummies'] = [x for x in cat_predictors if x in predictors_selected['ST_inter_dummies']]

predictors_selected['ST_inter_dummies']

['sq_mt_built',

'is_exterior',

'floor',

'n_bathrooms',

'house_type',

'energy_certificate',

'has_parking',

'has_lift']

interactions_selected['ST_inter_dummies']

[('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift')]

# Full model - interactions

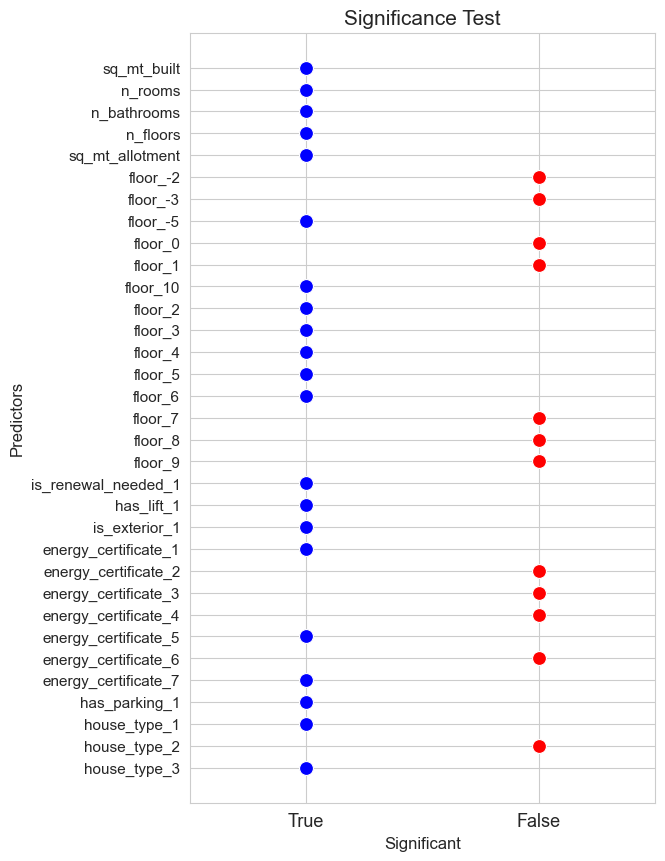

significant_pred_model_inter_ST, not_significant_pred_model_inter_ST = significant_test(model=full_model_inter, alpha=0.05, figsize=(6,7))

predictors_selected['ST_inter'] = [x for x in significant_pred_model_inter_dummies_ST if ':' not in x]

interactions_selected['ST_inter'] = [(x.split(':')[0], x.split(':')[1]) for x in significant_pred_model_inter_dummies_ST if ':' in x]

pred_to_dummies['ST_inter'] = None

predictors_selected['ST_inter']

['sq_mt_built',

'is_exterior',

'floor',

'n_bathrooms',

'house_type',

'energy_certificate',

'has_parking',

'has_lift']

interactions_selected['ST_inter']

[('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift')]

# Full model - dummies

significant_pred_model_dummies_ST, not_significant_pred_model_dummies_ST = significant_test(model=full_model_dummies, alpha=0.05, figsize=(6,10))

significant_pred_model_dummies_ST = recognition(significant_pred_model_dummies_ST)

not_significant = recognition(not_significant_pred_model_dummies_ST)

not_significant_pred_model_dummies_ST = np.array([x for x in not_significant if x not in significant_pred_model_dummies_ST])

predictors_selected['ST_dummies'] = significant_pred_model_dummies_ST

interactions_selected['ST_dummies'] = None

pred_to_dummies['ST_dummies'] = [x for x in cat_predictors if x in predictors_selected['ST_inter_dummies']]

predictors_selected['ST_dummies']

array(['sq_mt_allotment', 'sq_mt_built', 'n_floors', 'n_bathrooms',

'floor', 'is_renewal_needed', 'is_exterior', 'energy_certificate',

'house_type', 'has_parking', 'has_lift', 'n_rooms'], dtype='<U18')

interactions_selected['ST_dummies']

# Full model - not interactions - not dummies

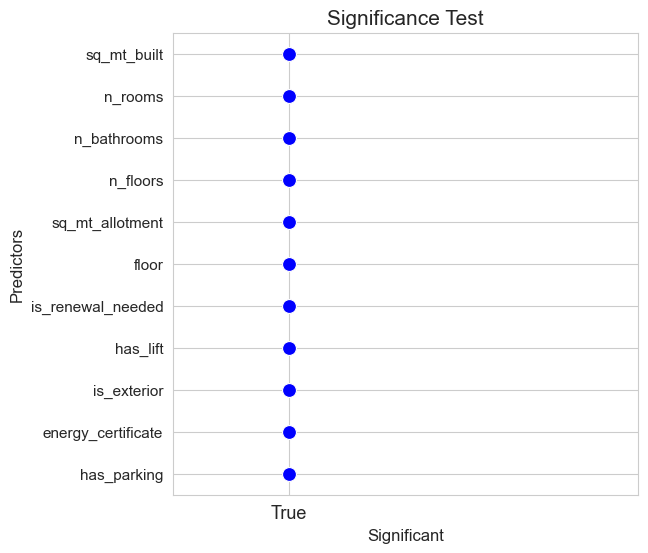

significant_pred_model_basic_ST, not_significant_pred_model_basic_ST = significant_test(model=full_model_basic, alpha=0.05, figsize=(6,6))

predictors_selected['ST_basic'] = significant_pred_model_basic_ST

interactions_selected['ST_basic'] = None

pred_to_dummies['ST_basic'] = None

predictors_selected['ST_basic']

array(['sq_mt_built', 'n_rooms', 'n_bathrooms', 'n_floors',

'sq_mt_allotment', 'floor', 'is_renewal_needed', 'has_lift',

'is_exterior', 'energy_certificate', 'has_parking'], dtype=object)

Likelihood Ratio Test#

Deviance

Given an statistical regression model \(M\), such as Poisson regression model, its deviance is defined as:

Where \(\mathcal{L}(\widehat{\beta}_0, \widehat{\beta})\) is the estimated Likelihood function of the model.

The deviance is a measure of how well the model is fitting the training data, so, is a measure of goodness of fit of the model.

Properties:

\(D(M)\in [0, \infty)\)

The larger \(D(M)\), the worse \(M\) fits the training data.

The smaller \(D(M)\), the better \(M\) fits the training data.

The null model \(M_0\) (the one that doesn’t include predictors) has the maximum deviance.

The classic determination coefficient \(R\)-square can be obtain through the deviance as \(\hspace{0.05cm}R^2(M) = 1 - \dfrac{D(M)}{D(M_0)}\)

Likelihood Ratio Test as significance test

Originally the Likelihood ratio test is a test to compare the goodness of fit of different nested models, but in this section we are going to adapt it to be a significance test for the predictors.

Given two nested models \(M_p\), \(M_{p-1}\) such that \(M_p\) is the full model (includes the \(p\) available predictors) and \(M_{p-1}\) is the same model but without the predictor \(X_j\).

The significant test for predictor \(X_j\) can be perform as a Likelihood Ratio Test:

\begin{cases} H_0 : M_{p-1} \ H_1 : M_p \end{cases}

Statistic:

p-value:

Decision rule:

If \(pvalue < \alpha \hspace{0.1cm} \Rightarrow\hspace{0.1cm}\) Reject \(H_0 \hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) \(M_p\) fits better the training data than \(M_{p-1}\) \(\hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) predictor \(\mathcal{X}_j\) is significative to explain the response.

If \(pvalue \geq \alpha \hspace{0.1cm} \Rightarrow\hspace{0.1cm}\) Not Reject \(H_0 \hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) \(M_{p-1}\) fits better the training data than \(M_{p}\) \(\hspace{0.1cm}\Rightarrow\hspace{0.1cm}\) predictor \(\mathcal{X}_j\) is not significative to explain the response.

Let’s implements the Likelihood Test Ratio as significance test in Python:

def LRT(full_model, predictor_to_test) :

X_full = full_model.X

Y = full_model.Y

interactions = full_model.interactions_to_add

pred_to_dummies = full_model.pred_to_dummies

predictors = X_full.columns.tolist().copy()

if predictor_to_test in predictors:

predictors_reduced = [x for x in predictors if x != predictor_to_test]

interactions_reduced = [(quant, cat) for (quant, cat) in interactions if cat != predictor_to_test and quant != predictor_to_test] if interactions is not None else None

pred_to_dummies_reduced = [x for x in pred_to_dummies if x != predictor_to_test] if pred_to_dummies is not None else None

elif predictor_to_test in interactions:

predictors_reduced = predictors

interactions_reduced = [(quant, cat) for (quant, cat) in interactions if (quant, cat) != predictor_to_test]

pred_to_dummies_reduced = pred_to_dummies

reduced_model = linear_model(Y=Y, X=X_full[predictors_reduced])

reduced_model.fit(pred_to_dummies=pred_to_dummies_reduced, interactions_to_add=interactions_reduced)

loglike_full = full_model.linear_fit.llf

loglike_reduced = reduced_model.linear_fit.llf

deviance_full = -2*loglike_full

deviance_reduced = -2*loglike_reduced

LRT_ = deviance_reduced - deviance_full

df_full = full_model.linear_fit.df_model # number of coefficients of full model

df_reduced = reduced_model.linear_fit.df_model # number of coefficients of reduced model

pvalue = stats.chi2.sf(LRT_, df_full-df_reduced)

return pvalue

def LTR_significant_test(full_model, alpha=0.05, figsize=(7,7)) :

if full_model.interactions_to_add is not None :

predictors_to_test = full_model.X.columns.tolist() + full_model.interactions_to_add

else:

predictors_to_test = full_model.X.columns.tolist()

pvalue = dict()

for predictor in predictors_to_test :

pvalue[predictor] = LRT(full_model, predictor_to_test=predictor)

predictors_tested = np.array([str(x) for x in pvalue.keys()])

pvalues = np.array([x for x in pvalue.values()])

significance_results = pvalues < alpha

significant_predictors = predictors_tested[significance_results==True]

not_significant_predictors = predictors_tested[significance_results==False]

significance_test_results_str = np.array([str(x) for x in significance_results])

plt.figure(figsize=figsize)

ax = sns.scatterplot(x=significance_test_results_str, y=predictors_tested, color='red', s=100)

ax = sns.scatterplot(x=significance_test_results_str[significance_results==True],

y=predictors_tested[significance_results==True], color='blue', s=100)

plt.title('Significance Test - LRT', size=15)

ax.set_ylabel('Predictors', size=12)

ax.set_xlabel('Significant', size=12)

plt.xticks(fontsize=11)

plt.yticks(fontsize=11)

ax.set_xlim(-0.5, 1.5)

plt.show()

return significant_predictors, not_significant_predictors

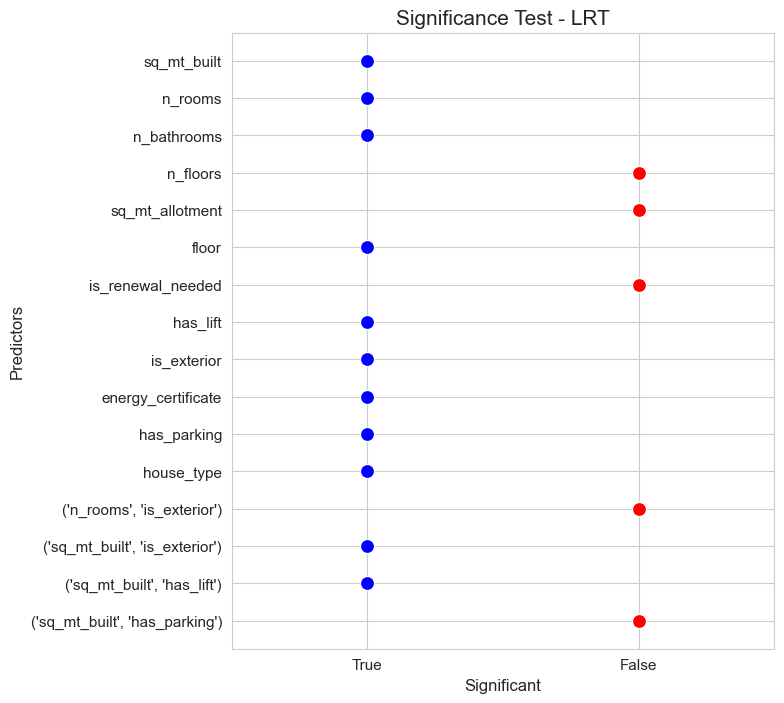

# Full model LRT - interactions - dummies

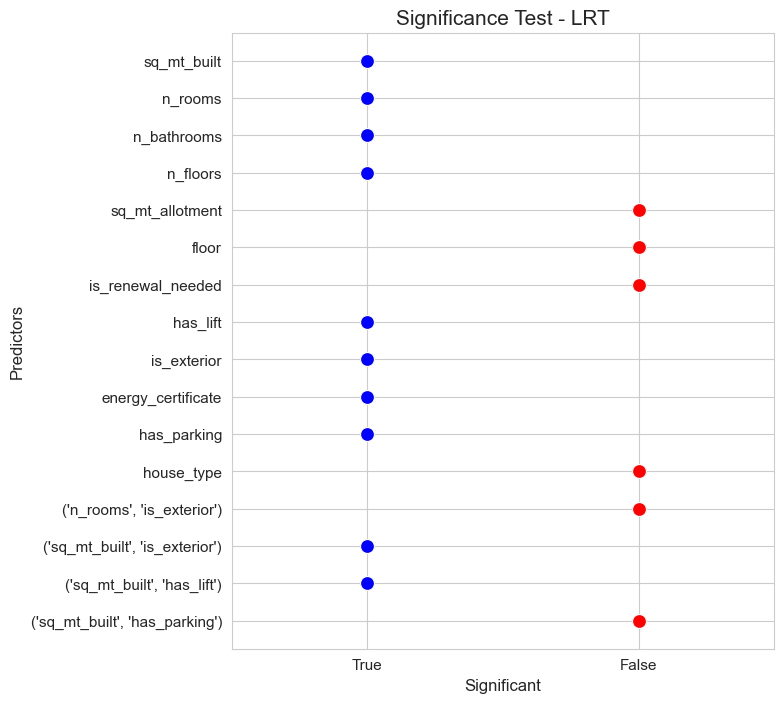

significant_pred_model_inter_dummies_LRT, not_significant_pred_model_inter_dummies_LRT = LTR_significant_test(full_model=full_model_inter_dummies,

alpha=0.05, figsize=(7,8))

significant_pred_model_inter_dummies_LRT

array(['sq_mt_built', 'n_rooms', 'n_bathrooms', 'floor', 'has_lift',

'is_exterior', 'energy_certificate', 'has_parking', 'house_type',

"('sq_mt_built', 'is_exterior')", "('sq_mt_built', 'has_lift')"],

dtype='<U30')

not_significant_pred_model_inter_dummies_LRT

array(['n_floors', 'sq_mt_allotment', 'is_renewal_needed',

"('n_rooms', 'is_exterior')", "('sq_mt_built', 'has_parking')"],

dtype='<U30')

predictors_selected['LRT_inter_dummies'] = [x for x in significant_pred_model_inter_dummies_LRT if not x[0] == '(']

interactions_selected['LRT_inter_dummies'] = [ast.literal_eval(x) for x in significant_pred_model_inter_dummies_LRT if x[0] == '(']

pred_to_dummies['LRT_inter_dummies'] = [x for x in cat_predictors if x in predictors_selected['LRT_inter_dummies']]

predictors_selected['LRT_inter_dummies']

['sq_mt_built',

'n_rooms',

'n_bathrooms',

'floor',

'has_lift',

'is_exterior',

'energy_certificate',

'has_parking',

'house_type']

interactions_selected['LRT_inter_dummies']

[('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift')]

# Full model - interactions

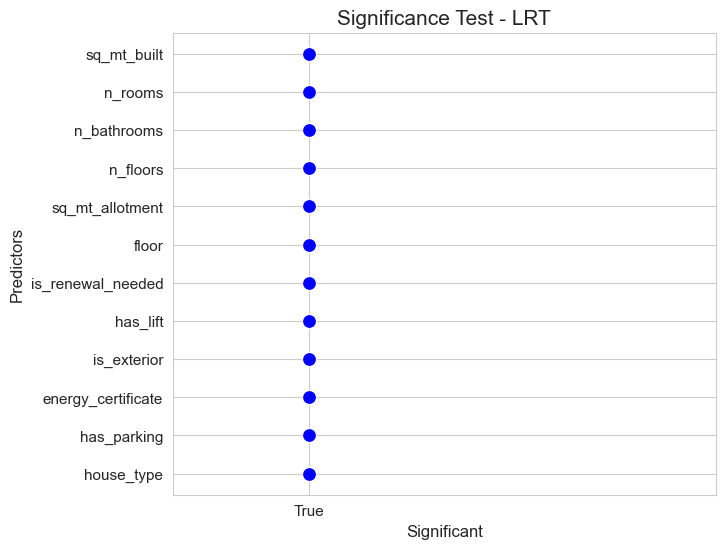

significant_pred_model_inter_LRT, not_significant_pred_model_inter_LRT = LTR_significant_test(full_model=full_model_inter, alpha=0.05, figsize=(7,8))

predictors_selected['LRT_inter'] = [x for x in significant_pred_model_inter_LRT if not x[0] == '(']

interactions_selected['LRT_inter'] = [ast.literal_eval(x) for x in significant_pred_model_inter_LRT if x[0] == '(']

pred_to_dummies['LRT_inter'] = None

predictors_selected['LRT_inter']

['sq_mt_built',

'n_rooms',

'n_bathrooms',

'n_floors',

'has_lift',

'is_exterior',

'energy_certificate',

'has_parking']

interactions_selected['LRT_inter']

[('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift')]

# Full model - dummies

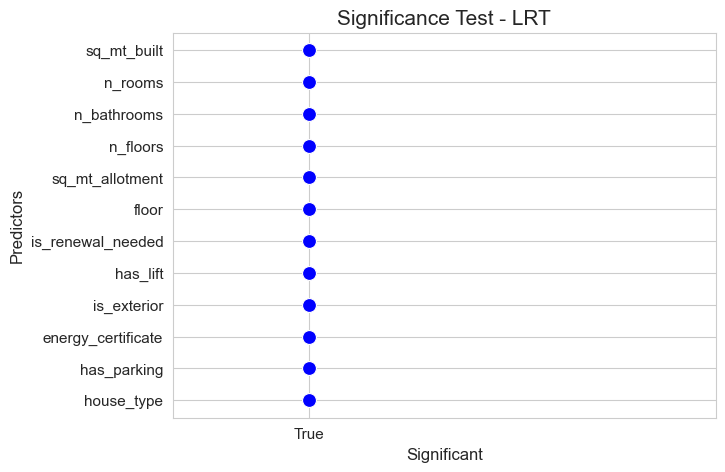

significant_pred_model_dummies_LRT, not_significant_pred_model_dummies_LRT = LTR_significant_test(full_model=full_model_dummies,

alpha=0.05, figsize=(7,6))

predictors_selected['LRT_dummies'] = significant_pred_model_dummies_LRT

interactions_selected['LRT_dummies'] = None

pred_to_dummies['LRT_dummies'] = None

predictors_selected['LRT_dummies']

array(['sq_mt_built', 'n_rooms', 'n_bathrooms', 'n_floors',

'sq_mt_allotment', 'floor', 'is_renewal_needed', 'has_lift',

'is_exterior', 'energy_certificate', 'has_parking', 'house_type'],

dtype='<U18')

# Full model - basic (not interactions - not dummies)

significant_pred_model_basic_LRT, not_significant_pred_model_basic_LRT = LTR_significant_test(full_model=full_model_basic,

alpha=0.05, figsize=(7,5))

predictors_selected['LRT_basic'] = significant_pred_model_basic_LRT

interactions_selected['LRT_basic'] = None

pred_to_dummies['LRT_basic'] = None

predictors_selected['LRT_basic']

array(['sq_mt_built', 'n_rooms', 'n_bathrooms', 'n_floors',

'sq_mt_allotment', 'floor', 'is_renewal_needed', 'has_lift',

'is_exterior', 'energy_certificate', 'has_parking', 'house_type'],

dtype='<U18')

Predictors selection based on predictive performance#

The idea is to consider the predictors as hyper-parameters of the model and optimize them using algorithms like grid search and cross validation.

Train-Train - Train-Validate split#

Since we need to test the predictive performance of the models we need to split train partition in train-train (train2) to train the models and train-validate (val) to test them.

We don’t use test partition in this case since this task implies taking decisions regarding the predictive modeling process and these decisions should be done with the training data, otherwise this can lead to data leakage.

The test partition will only be used to estimate the future performance of our final model.

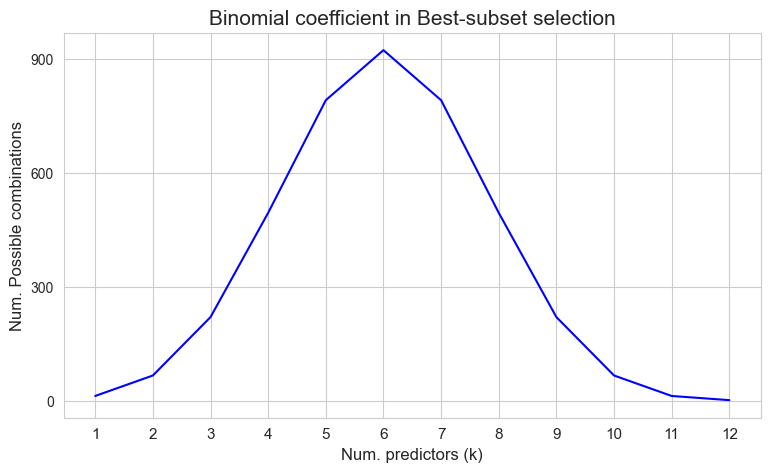

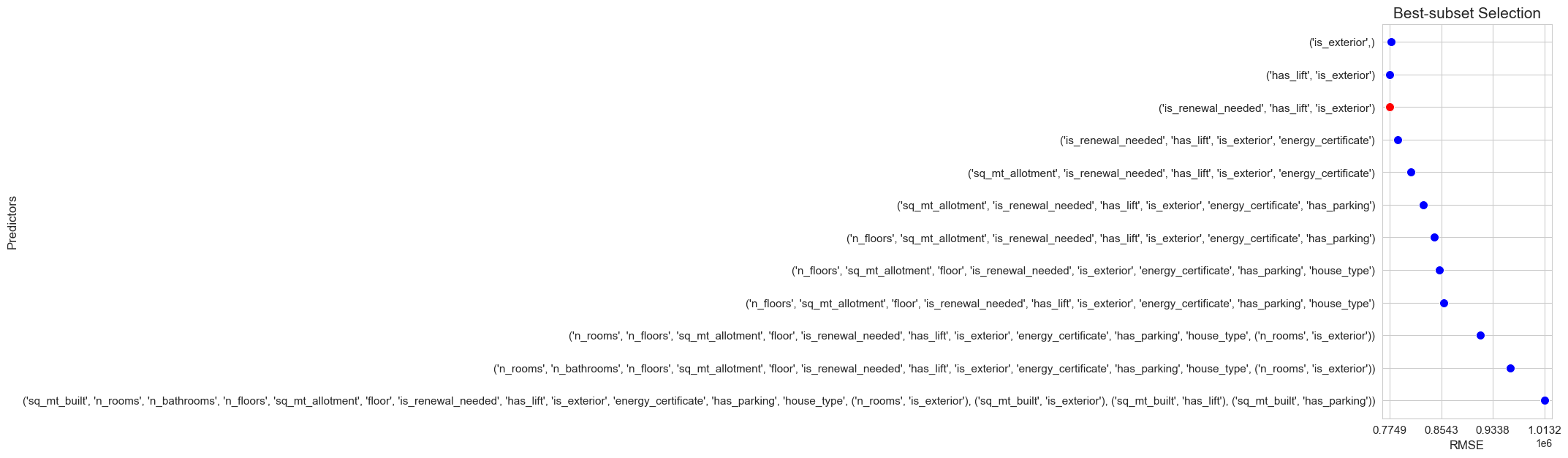

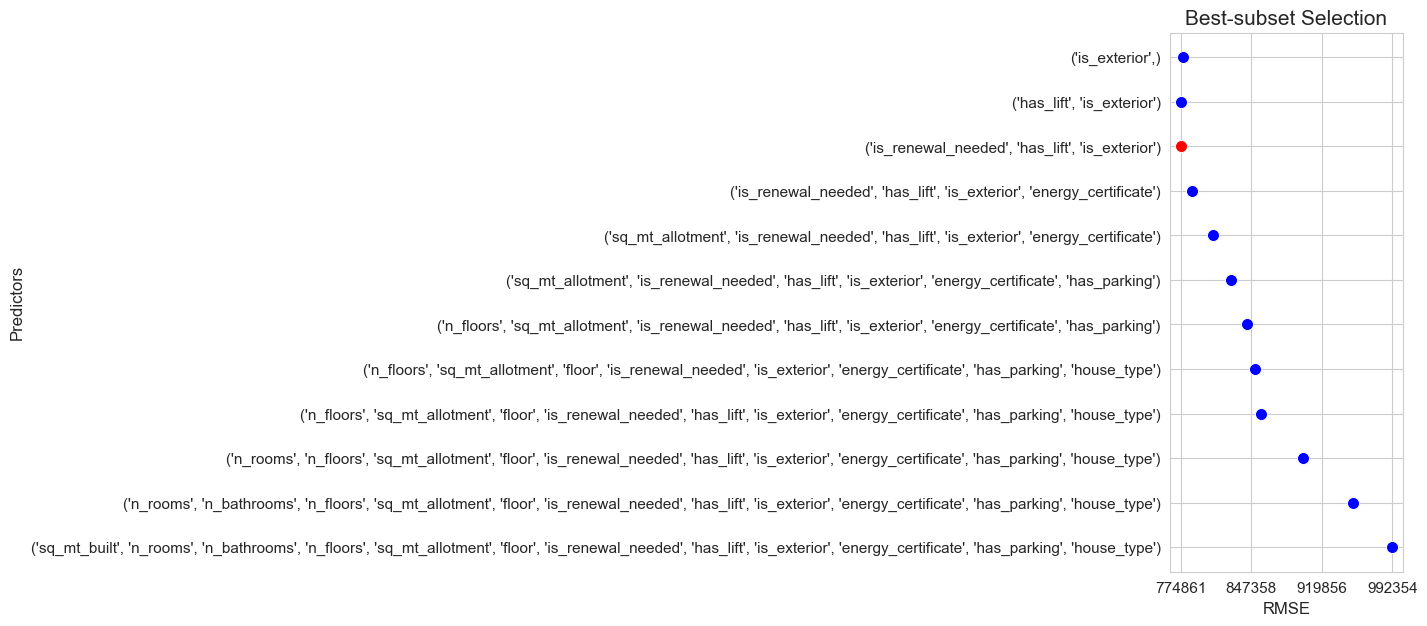

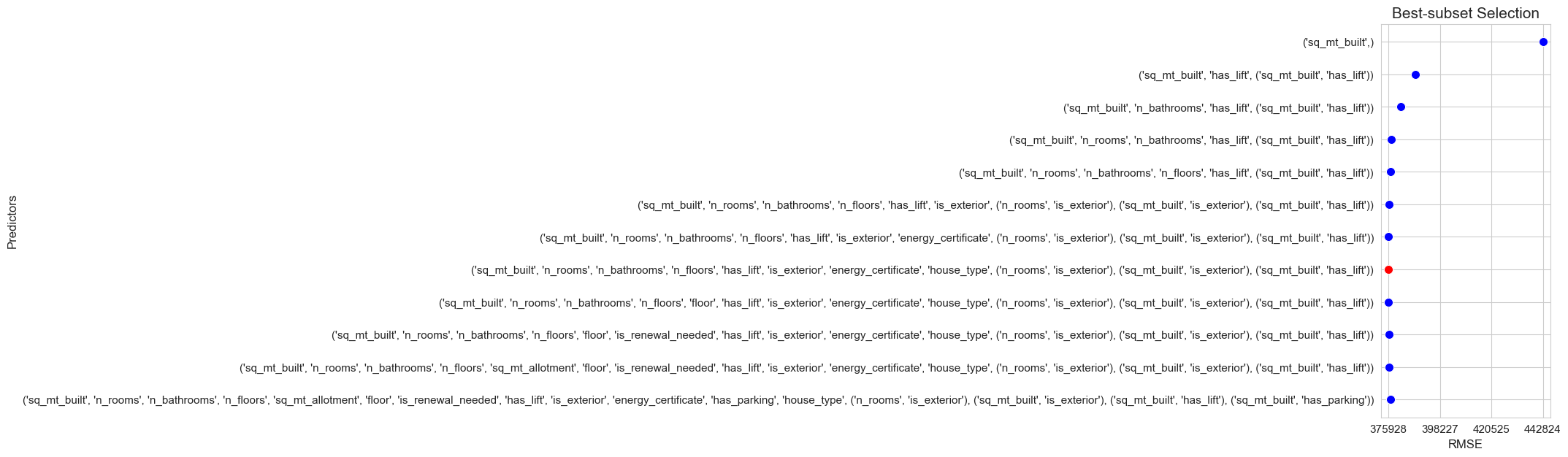

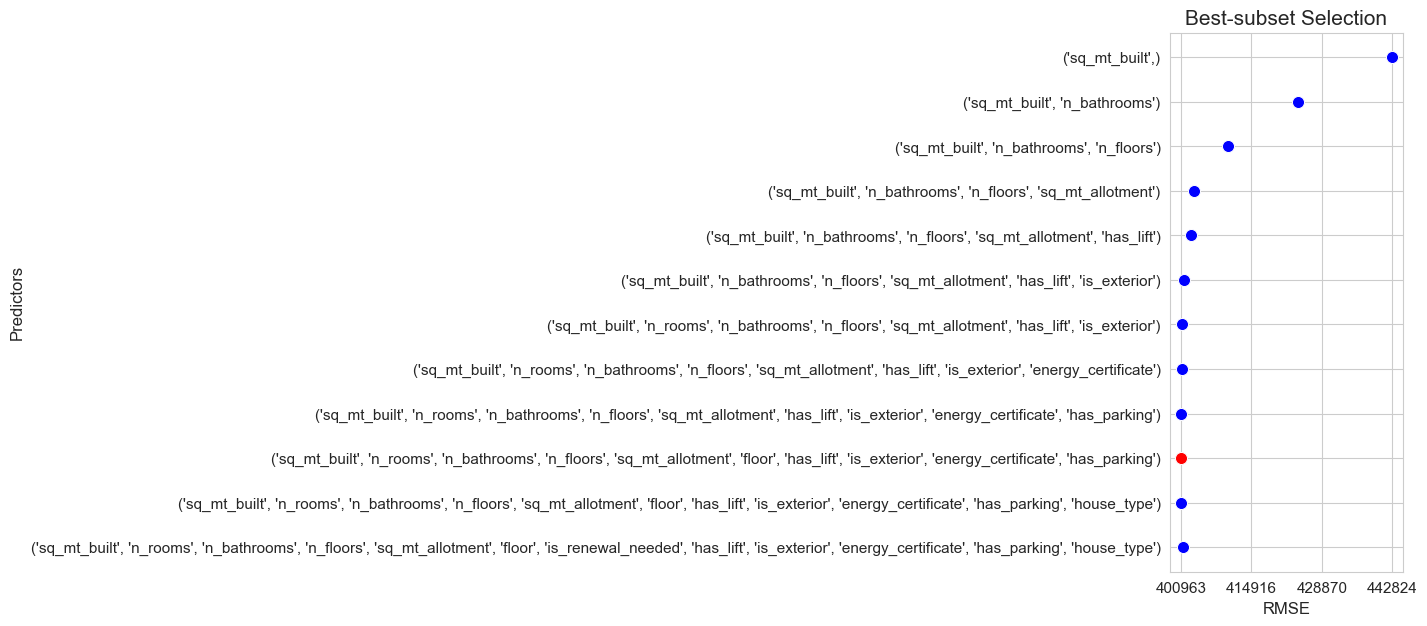

Best subset selection algorithm#

Best subset selection algorithm :

We have \(p\) predictors.

We train all the possible linear models with \(1\) predictor, and select the one with less test prediction error computed by simple validation \(\Rightarrow M_1^*\)

We train all the possible linear models with \(2\) predictor, and select the one with less test prediction error computed by simple validation \(\Rightarrow M_2^*\)

\(\dots\)We train all the possible linear models with \(p-1\) predictor, and select the one with less test prediction error computed by simple validation \(\Rightarrow M_{p-1}^*\)

We train the full linear model \(\Rightarrow M_{p}\)

Among \(M_1^*, M_2^*,\dots, M_{p-1}^*, M_p\) we select the one with less test prediction error, and it is consider the best Poisson model according to best subset selection algorithm.

This method is feasible in this case, because as we saw before, the number of possible linear regression models that can be trained with all the possible subsets of the \(p=12\) predictors is \(4095\), which is acceptable computationally with the statsmodels implementation of the linear regression model.

p=len(predictors)

binom_values = [binom(p=len(predictors), k=k) for k in np.arange(1,p+1)]

plt.figure(figsize=(9, 5))

ax = sns.lineplot(y=binom_values, x=np.arange(1,p+1), color='blue')

ax.set_ylabel('Num. Possible combinations', size=12)

ax.set_xlabel('Num. predictors (k)', size=12)

plt.xticks(np.arange(1,p+1), fontsize=11)

plt.yticks(np.arange(0,1000, 300))

plt.title('Binomial coefficient in Best-subset selection', size=15)

plt.show()

def simple_validation(X, Y, train_size, seed, pred_to_dummies, interactions_to_add):

X_train, X_test, Y_train, Y_test = train_test_split(X, Y, train_size=train_size, random_state=seed)

model = linear_model(Y=Y_train, X=X_train)

model.fit(pred_to_dummies=pred_to_dummies, interactions_to_add=interactions_to_add)

Y_test_hat = model.predict(X_test)

RMSE = np.sqrt(np.mean((Y_test - Y_test_hat)**2))

return RMSE

def best_subset_selection(X, Y, pred_to_dummies=None, interactions=None, train_size=0.75, seed=123) :

results = dict()

RMSE = dict()

predictors = X_train.columns.tolist()

n_iter = len(predictors)

for iter in range(1, n_iter+1) :

predictors_combinations = []

predictors_combinations = list(combinations(predictors, iter))

for predictors_combi in predictors_combinations:

pred_to_dummies_reduced = [x for x in pred_to_dummies if x in list(predictors_combi)] if pred_to_dummies is not None else None

interactions_reduced = [(quant, cat) for (quant, cat) in interactions if cat in list(predictors_combi) and quant in list(predictors_combi)] if interactions is not None else None

RMSE[predictors_combi] = simple_validation(X=X[list(predictors_combi)], Y=Y, train_size=train_size, seed=seed,

pred_to_dummies=pred_to_dummies_reduced, interactions_to_add=interactions_reduced)

RMSE_predictors = [x for x in RMSE.keys()]

RMSE_values = np.array([x for x in RMSE.values()])

best_predictors = RMSE_predictors[np.argsort(RMSE_values)[0]]

best_interactions = tuple([(quant,cat) for (quant,cat) in interactions if quant in list(best_predictors) and cat in list(best_predictors)]) if interactions is not None else None

if best_interactions is not None:

results[best_predictors + best_interactions] = np.min(RMSE_values)

else:

results[best_predictors] = np.min(RMSE_values)

# Clean the dictionary

RMSE = dict()

return results

# Models with: dummies - interactions

results = best_subset_selection(X=X_train, Y=Y_train, train_size=0.75, seed=123,

pred_to_dummies=cat_predictors,

interactions=[('n_rooms', 'is_exterior'), ('sq_mt_built', 'is_exterior'), ('sq_mt_built', 'has_lift'), ('sq_mt_built', 'has_parking')])

result_predictors = [x for x in results.keys()]

result_predictors_str = np.array([str(x) for x in results.keys()])

result_score = np.array([x for x in results.values()])

best_pred_bestsubset_inter_dummies_str = result_predictors_str[np.argsort(result_score)[0]]

best_pred_bestsubset_inter_dummies = list(result_predictors[np.argsort(result_score)[0]])

best_RMSE_bestsubset_inter_dummies = np.min(result_score)

predictors_selected['BestSubset_inter_dummies'] = [x for x in best_pred_bestsubset_inter_dummies if not isinstance(x,tuple)]

interactions_selected['BestSubset_inter_dummies'] = [ast.literal_eval(x) for x in best_pred_bestsubset_inter_dummies if isinstance(x,tuple)]

pred_to_dummies['BestSubset_inter_dummies'] = [x for x in cat_predictors if x in predictors_selected['BestSubset_inter_dummies']]

predictors_selected['BestSubset_inter_dummies']

['is_renewal_needed', 'has_lift', 'is_exterior']

interactions_selected['BestSubset_inter_dummies']

[]